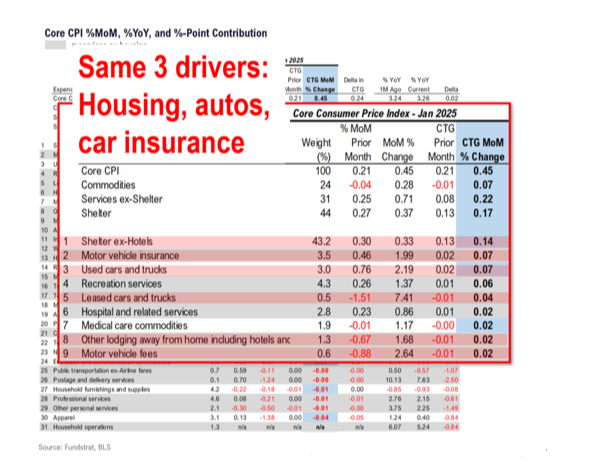

Last Wednesday, January’s consumer price index report was hotter than expected, causing initial market volatility. Core CPI, which excludes volatile food and energy prices, rose 0.45% on a month-over-month basis.

However, despite the initial market selloff, equities recovered throughout the day. Once again, we see continued investor resilience, and we think there are six reasons for it.

Rise May Not Be Sustainable

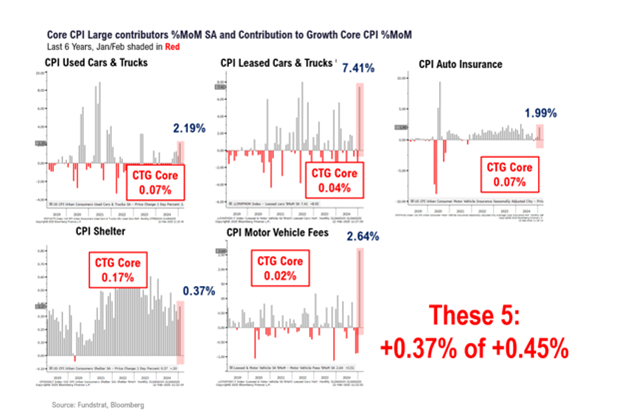

First, investors clearly were skeptical about the CPI data. They questioned whether the inflation spike was real or just seasonal adjustments. Consider how the stubborn housing, auto insurance, and used vehicles categories accounted for 0.37% of the 0.45% increase:

This suggests the rise may not be sustainable. In fact, we wrote about a similarly hot inflation report last February. Early in the year often produces price jumps, but they’re usually not trends which will most likely be supported by a tame January PCE.

Federal Reserve Response

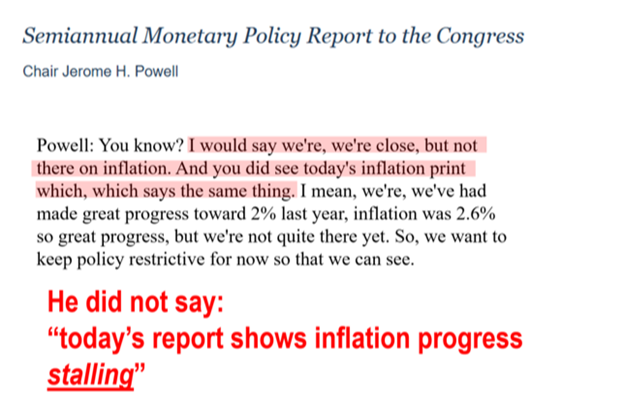

The Fed response was rather muted:

It’s important to note that while Chair Jerome Powell acknowledged the report, he clearly doesn’t believe progress on inflation has stalled or faded.

Corporate Fundamental Strength

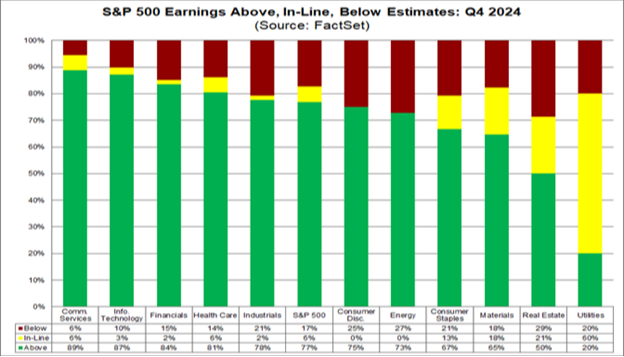

Earnings move stocks, and earnings remain extraordinarily strong. This earnings season so far has been a showcase of corporate fundamental strength.

As of last week, 77% of S&P 500* companies reported positive earnings surprises, beating the 10-year average of 75:

Plus, the companies reporting earnings surprises are beating estimates by 7.5%, which bests the 10-year average of 6.7%.

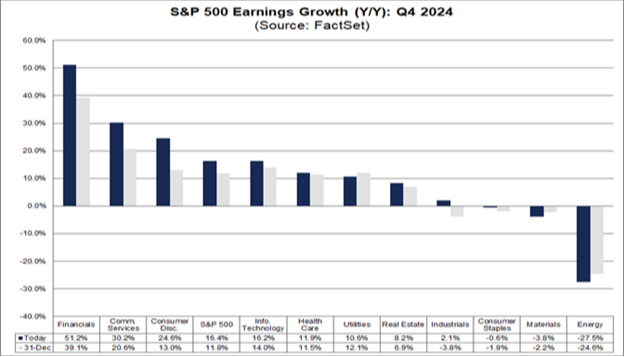

Even more remarkable, the blended earnings growth rate for the quarter so far is 16.4% – much higher than the 11.8% estimate:

If that 16.4% rate prevails, it will mark the highest year-over-year earnings growth rate since late 2021.

Investors Already De-Risked

As we discussed before, individual investor sentiment was already bearish, having collapsed in December and last month. Alas, those investors already de-risked.

That cushioned last week’s market reaction.

“Buy the Dip”

Like in 2023 and 2024, the “buy the dip” trend has continued to show resiliance.

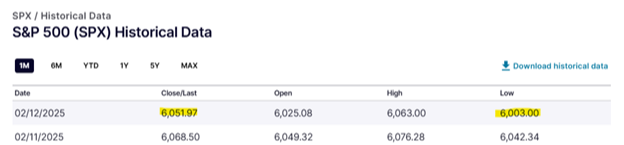

After Wednesday’s CPI report, we saw the S&P 500 drop 65.50 points at its lowest. But then it reversed course, closing the day down only 16.53 points:

This is the third straight year of investors scooping up quick market dips.

Proof of the Continued Rebound

After the CPI report last Wednesday, the next day the producer price index report was released. It came in line with expectations (0.3% rise), which contributed to a drop in Treasury yields and helped markets open positively.

Last Thursday’s PPI wasn’t a reason stocks bounced back, but rather further support for the continued rebound in equities and a reason to keep going.

Despite a higher-than-expected CPI, investors encouragingly bought the dip. Truthfully, the Fed’s reaction matters more than one month’s data.

All-Weather Investing

It’s clear volatility is back, even with the bullish “buy the dip” prevailing mentality. This clearly affects interest rates, but we want to discuss why this bodes well for dividend equity investing.

This current environment brings back into focus a familiar playbook going back to 2022 and 2016-2020. As we gain more visibility, it’s likely 2025 will be choppier than the past couple of years, and this will showcase the strength of an all-weather investing strategy like dividend growth.

Eighth Wonder of the World

Albert Einstein once described compound interest as the eighth wonder of the world. We couldn't agree more.

This is even true when looking at the S&P 500. Since 1930, the index gained an average of 6.7% per year, excluding dividends. But when dividends were reinvested, it gained 10.4%.

This is a perfect example of the supercharging nature of long-term, compounding growth.

Since 2000, S&P 500 dividends alone have grown 6.9% per year. So, dividend growth can be a significant hedge against market volatility.

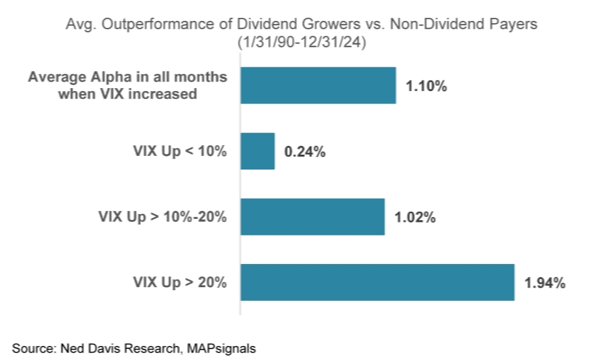

Since 1990, when the CBOE Volatility Index (VIX)#, often dubbed the market’s “fear gauge,” rose, dividend growers outgained non-dividend paying stocks:

Drilling even down even further, when VIX rose over 20%, dividend growers outperformed non-payers by almost 2%.

Times Have Changed

Bonds play a critical role in managing volatility and risk in investment portfolios, right? Well, we’d argue that times have changed, and smart investors need to change with them (rising long-term rates significantly pressured bond prices).

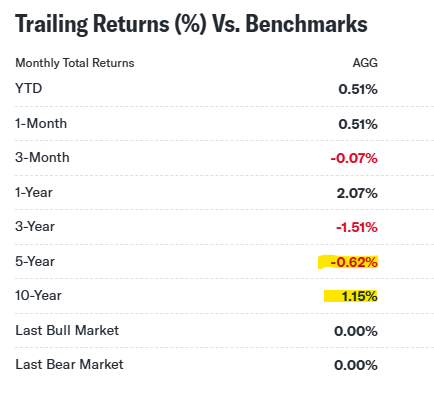

Using the exchange-traded fund iShares Core U.S. Aggregate Bond ETF (AGG) as a proxy, this leading U.S. fixed income benchmark produced -0.62% annualized total returns over the last five years, and only 1.15% annualized total returns over the past 10 years, respectively:

From the early 1980s through 2015 or so, bonds enjoyed an epic bull market. That party is over as bonds have been in a bear market for about a decade now.

What should income investors do instead for yield? In our opinion, look no further than dividend growth stocks.

Over the last 10 years, AGG rose a mere 13% versus 211% and 161% for the leading U.S. dividend growth and high dividend indices, respectively:

Continued Outperformance

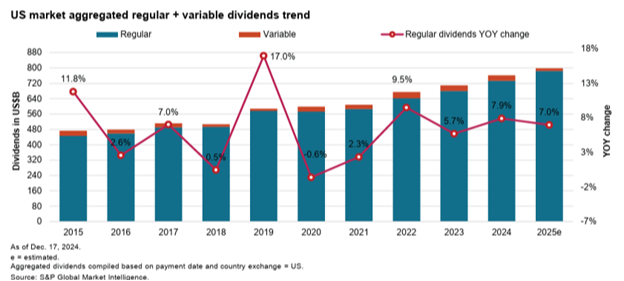

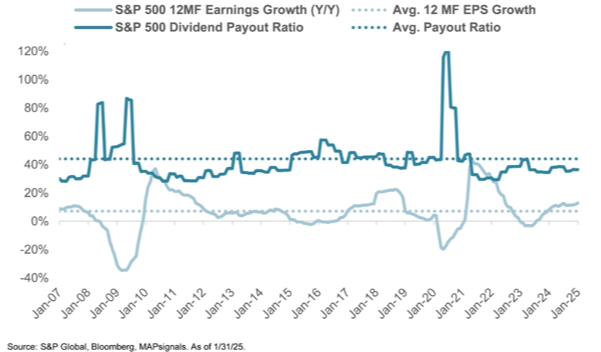

As we continue seeing record earnings (as shown above), it increasingly contributes to low payout ratios, which strengthens divided growth stocks. The 2025 forecast for the U.S. equity dividend growth in aggregate is expected to be 7% this year alone:

What’s driving this dividend growth bull market?

We’d point to record corporate profitability – dividends can't grow quickly if profits don't too. For the full year, S&P 500 earnings are expected to rise 13%, which is almost double the long-term average.

A great recent example was the January announcement by financial firm Blackstone increasing its dividend by 67%. The company now has a five-year average dividend increase rate of 15.5% per year.

Furthermore, we're seeing a record low payout ratio (i.e., the percentage of profits used to cover dividends) of 36%, which is well below the 45% long-term average:

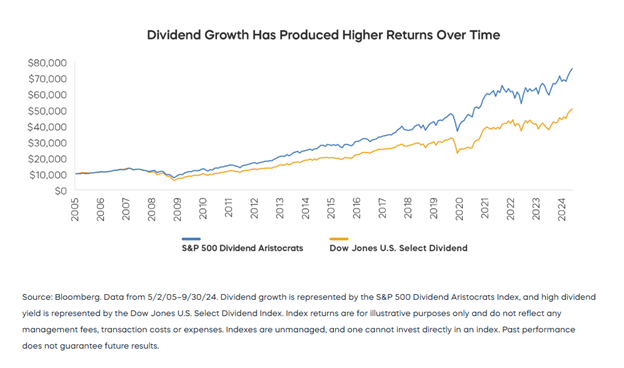

This supports continued outperformance of dividend growth stocks over time:

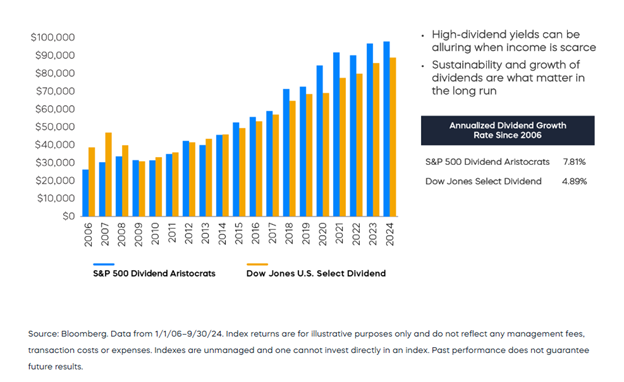

But let’s be clear: big yields alone are tempting to many investors but sky-high dividend yields often signal distress. So, it’s no surprise that dividend growth strategies consistently outperform their high dividend yield counterparts.

It’s because quality matters. Dividend growth stocks have produced higher overall returns on equity than high dividend stocks. This is even more important in today's environment, where uncertainty surrounding inflation and interest rates is rampant.

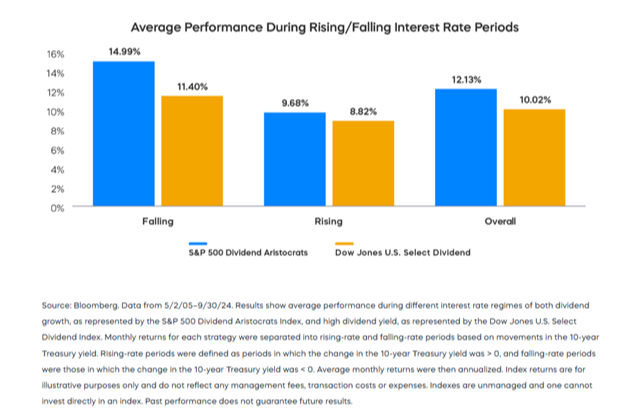

Importantly, dividend growth equities provide outsized returns whether rates are rising or falling:

High-quality dividend growth stocks are time tested:

They sustain in nearly all environments and have outperformed their high dividend counterparts.

* Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

*Past performance does not guarantee future results.

*Investing involves risk and you may incur a profit or loss regardless of strategy selected.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

# The CBOE Volatility Index is a measure of the short-term volatility of the S&P 500 indexes, indicating how quickly market sentiment changes and the level of investor confidence or fear in the market.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.