Last Tuesday produced the largest selloff in equities so far in 2024 after the January consumer price index report came in hot versus the consensus expectation (“core CPI” was up 0.39% versus a consensus of 0.30%). While the decline was seemingly significant, let’s remember it was a mild retracement requiring a collective effort from angry, bearish investors.

The S&P 500* fell to a level it hit four days prior although bounced back the next day:

While angry bears celebrated briefly, one thing we monitor did make us uncomfortable: the bond market selling off sharply. Big bond sales made yields jump (remember, bond prices and yields have an inverse relationship). As of this writing, the yield on the 10-year Treasury is back up around 4.3%:

We’ve been warning of near-term volatility, but we think this is an overreaction to a single inflation report. Why though?

Even after the report, overall inflation continues trending lower over time. But four specific areas are behind the latest uptick:

- Shelter costs – owners’ equivalent rent (OER) is proving to be sticky, though that’s temporary and a lagging data point.

- Auto insurance – costs jumped, but it won’t last forever as it is merely catching up.

- Miscellaneous personal services – a direct result of financial services costing more because stock prices increased (cyclical).

- Hospital services – the one possible concern as we are not certain yet the cause.

So, three of the four culprits are temporary and shouldn’t linger.

Drilling further into OER, Renaissance Macro Research showed how OER surged to 6.94% on a year-over-year basis while “rent of residence” fell to a pace of 4.4% on a year-over-year basis:

This is a significantly unusual divergence. History indicates that gap should close. If the supply of housing is the primary constraint, then keeping policy tight (i.e., higher interest rates) magnifies the issue.

Looking at the other stubborn inflation contributors, we’ve mentioned how auto insurance cost increases would be temporary in nature and a lagging inflation data point. Similarly, financial services costs rose because of higher stock prices, and we know markets are cyclical. Thus, we don’t think the downward trend in inflation will be halted.

“Core CPI” was up 0.39% month-over-month. Shelter costs contributed 0.26% to that growth, while auto insurance contributed 0.05%. Excluding those two items, which are lagging measures and temporary in nature, “core CPI” was up just 0.08%, or 0.96% annualized.

Also, the jump in miscellaneous personal services costs can largely be attributed to financial services costs rising. As previously mentioned, the driver behind that is stock price increases:

The bottom line is some investors are taking profits, which is healthy. We’ve mentioned early-year volatility before. Seeing it materialize doesn’t alter the pattern we expect for 2024:

But looking forward, let’s remember what’s going to impact markets. There are significantly more tailwinds than headwinds:

Now let’s turn to “big money” – the professional investors and institutions who move markets for a living. Looking at where we are today, it’s important to remember how markets move in cycles.

Our readers know of our friends at MAPsignals, who produce the Big Money Index (BMI), a 25-day moving average of “big money” investor buys and sells. MAPsignals also illustrated the cyclical nature of markets and what happens during each phase:

We’re currently near phase two right now. Buying has slowed. That, rather than a large increase in selling, has caused the BMI to fall out of overbought territory:

The massive December 2023 buying that pushed markets and the BMI higher has rolled out of the calculation. That’s why the index dipped. It’s clear from the data there’s been no increase in big selling yet:

Before the BMI nosedives and markets follow suit, there will need to be some convincing sell action. That’s not happening just yet. Also, since earnings season has been strong, downside volatility likely won’t materialize until earnings season is complete and there’s a lull in company-specific news. That could start in as early as a week or so.

How do you play a short-term, volatile dip once it reveals itself?

First and foremost, a big narrative last week after the inflation report was a change in expectations for the Federal Reserve’s seemingly imminent interest rate cuts. Falling rates and hopes for Fed cuts have been huge drivers of the most recent stock market rally.

But as our readers know, we’ve been firmly in the camp of cuts coming in the latter part of the second quarter this year, not in March. We think the most recent data supports this position. While rate cuts might be “delayed” in the eyes of the financial news media, the cuts won’t be denied forever.

Additionally, as mentioned above, we'll be keeping a close eye on our trusted BMI. The near-term dip indicates institutional investors have repositioned to short-term profit taking that also coincided with the recent inflation news. None of this was a surprise to us. We expected some volatility.

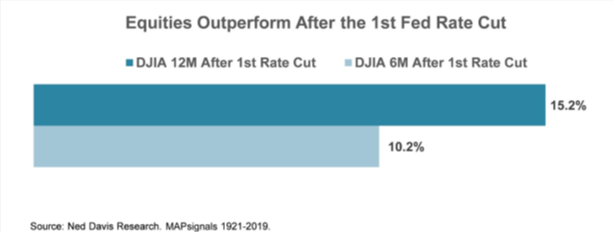

Inevitably, the Fed will start cutting rates. To prepare, we look at history. Since 1921, the Dow Jones Industrial Average# has produced 10.2% average gains in the six months after the first cut and 15.2% average jumps after 12 months (roughly 50.0% outperformance versus normal gains):

Drilling down more, some in the media continue to talk about a tech bubble. However, big tech’s 12-month forward earnings have been revised 15.6% higher since October versus a 2.5% upward revision for the S&P 500 in totality:

Tech’s valuation premium is easily justified. It will be the first sector we buy on any material short term weakness.

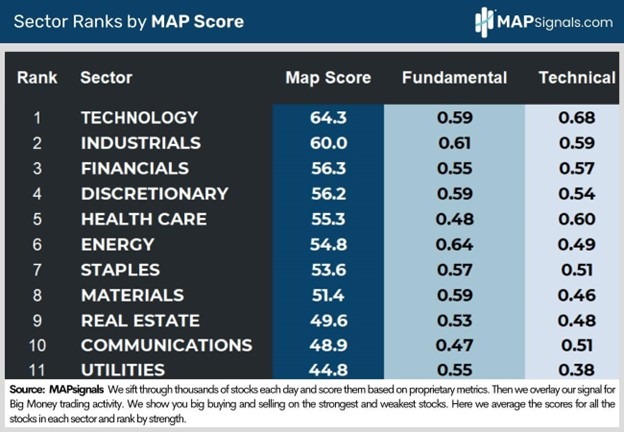

As for the rest of the market, interest-rate sensitive areas like regional banks, real estate, utilities, materials, and biotech are all lagging badly (see below). They’ll improve once the Fed pivots, but in the short term, we expect them to continue to underperform.

To summarize, the BMI falling from overbought is a mild concern. But let’s recognize the conflicting information under the surface. As always, we’ll trust data for conviction about near-term market prices. That said, our long-term narrative for 2024 remains the same.

*Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

# The Dow Jones Industrial Average is a stock market index of 30 prominent companies listed on stock exchanges in the U.S.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.