The past few weeks we’ve written about 2024, providing an early look into the year and the 12 charts of Christmas. Today we want to finalize our three-part 2024 series and outline Cornerstone’s full thesis for next year.

As we sit here today, we believe 2024 should present investors with more compelling opportunities than what’s been available the last couple of years. The primary reason is the Federal Reserve will likely cut interest rates in 2024 as inflation continues to nosedive towards the Fed’s “2.0% target.” This would be a significant catalyst for markets, so staying in equities should be a prudent choice.

If the Fed reverses its tightening, it will likely mean more than the so-called “Magnificent Seven” rallying. Narrow market focus was the theme of 2023, but in 2024 we think growth will broaden (we’re already seeing it now).

In our view, while vigilance is prudent the current landscape doesn't exhibit the same scale of systematic concerns as in 2001, 2007, or even 2022. We expect equities to beat consensus expectations in 2024 because:

- Base case: Inflation will keep falling, leading to faster-than-expected easing. That means no recession, though there may be weak jobs data in the first half of 2024.

- Key driver: Easing conditions will lead to lower interest rates and a rise in real consumer income.

- Earnings per share: We see 2024-25 EPS growth of 11.3% and 8.3% for the S&P 500*, leading to EPS of $240-260 driven by cyclical EPS recovery.

- Price-earnings ratio: We see P/E expanding in 2024 towards 20-to-1. While many argue for valuation compression, since 1937 the highest P/E ratios occur when yields are 3.5%-5.5%.

Let’s discuss why rate cuts are potentially the biggest tailwind for stocks. Should they occur – and we think they will – it will be because inflation is near 2.0%, meaning consumer prices have come down significantly. The consensus expectation is that personal consumption expenditures (PCE) will dip to 2.5% by the fourth quarter:

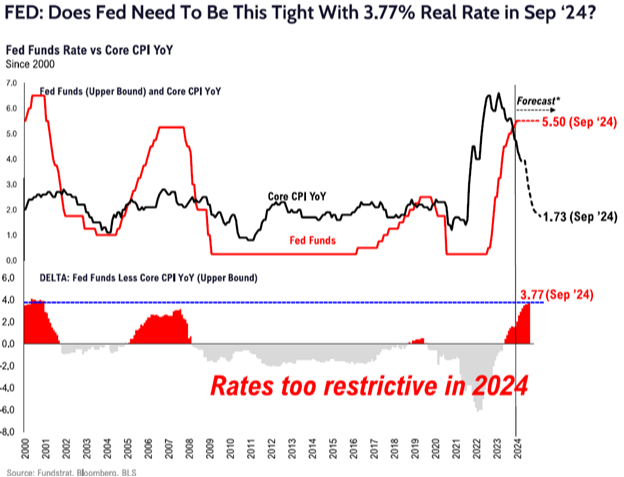

We’re slightly more bullish. We think the core consumer price index (“core CPI”) could drop to less than 2.0% by the third quarter of next year:

Should that occur, current Fed rates would be too restrictive from a spread standpoint. Fed rate cuts depend on three things:

- Confidence in the return to 2.0% inflation.

- A sufficiently weakened economy needing support.

- Free market consensus forcing rate consideration.

We think these conditions will likely be met at some point in the second quarter of next year. How will markets react? Over the past six rate cutting cycles since 1984, the S&P 500’s median return was 8.7% during the six months leading up to the first cut:

Thus, market returns should advance as we progress through the first half of 2024. Also, the median duration of the Fed holding rates before initiating cuts is about six months. In those scenarios, the S&P 500 historically delivers an average return of 9.2%:

The bottom line is that the market is likely to welcome the first rate cut and will price it in preemptively, before the actual cut. That would prolong the current rally. With this tailwind in focus, let’s turn to how this will affect equity valuations and the market in 2024.

The current 2024 bottom-up consensus earnings estimate for the S&P 500 rose since mid-November to $246. But if the Fed cuts rates, we see upside in both multiples and EPS.

Even without rate cuts, based on the current earnings increase expectation, the 2025 bottom-up consensus EPS estimate would be $275. That suggests further equity upside at the fair value equation.

Knowing that markets look forward and that the range of EPS for 2024-25 is $246-$275, our expectation for the S&P 500 in 2024 is a 20-to-1 P/E ratio based on EPS of $250-$260. We expect ample market breadth:

Therefore, our S&P 500 price target range is 5,000-5,200. We lean to the higher end, putting us above consensus expectations:

With our year-end target of 5,200, which represents a 12.0%-15.0% return from today, we thought it was right to break 2024 into two halves due to the quickly changing economic dynamics, especially of late. We're basing our thesis on a comprehensive range of macro factors, including inflation, mortgage rates, profits, and more. They support our cyclical growth thesis for 2024:

Headwinds and Bear Narratives

Now, that’s a lot of good news. But let’s also introduce some realism into the thesis – headwinds and bearish media narratives exist, and they can derail progress.

Since 2023 has been extraordinarily strong from a return standpoint, that means 2024 will be weak, right? Well, half the time since 1950 stocks gain more than 10.0% after a previous annual gain of 15.0% or more, and returns are positive 71.0% of the time:

As a result, Treasury auction sizes are expected to increase. This will be something we continue to watch closely. It could be another idiosyncratic reason interest rates will come down because the Fed may need to hedge against our nation’s debt interest payment risk.

Moving to commercial real estate, higher rates coupled with declining property valuations have impacted this market, specifically the office sector. Between 2024 and 2025, approximately $1.2 trillion of commercial real estate debt is set to mature. That’s close to 25.0% of all commercial real estate debt, which intensifies concerns about refinancing:

Still, we don't believe a declining office real estate market will “break” the economy. Just 10.0% of U.S. office buildings account for 80.0% of the occupancy losses from 2020-22. Realistically, office assets are a small share of the overall pie:

Additionally, while offices account for 27.0% of the current $636 billion commercial debt outstanding, this is materially smaller than in 2007, when doomed residential mortgage-backed securities accounted for $2.7 trillion. Office real estate’s overall effect on the macroeconomy isn’t as big.

Another potential pain point is U.S. consumer debt. But from a historical perspective, household leverage isn’t that high, even with the recent increase:

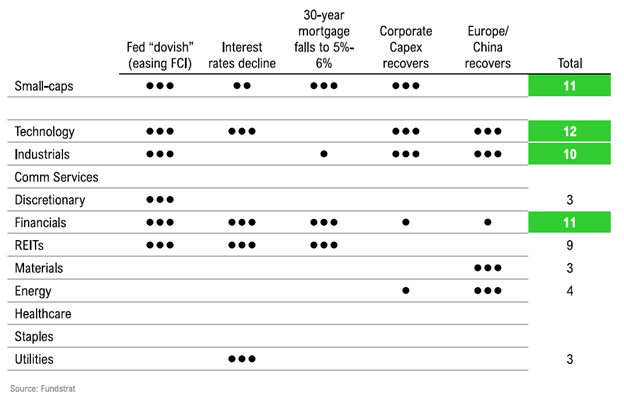

There you have it: we’ve explored the current underlying data that provides confidence in another strong equity market and acknowledged strong potential risks. Let’s finish by highlighting sectors that should be the greatest beneficiaries of this macro environment. Our best areas of focus will be small-caps, technology, industrials, and financials:

Headwinds exist, but the supporting data is strong. Our 2024 verdict? Strap in and get ready for another new year. Hopefully this time around we can achieve investing victory without enduring all the chaos and volatility of 2023.

Happy New Year!

*Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.