Welcome to 2024!

After such a volatile year, we expect 2024 to be easier to navigate comparatively, with positive tailwinds compounding throughout the year. Strong data continues to be the story, at least for data-driven organizations.

At the most macro level, we can see market strength continuing as the trusty Big Money Index (BMI) from MAPsignals has risen (and holding) to a still-overbought 91.0% as of this writing. The BMI is a netted 25-day moving average of “big money” professional investor buys and sells, and it’s not cooling off:

This shouldn’t be too surprising, given a powerfully positive combination of fundamental tailwinds:

- Falling inflation.

- Dovish Federal Reserve.

- Falling interest rates, which help consumers, corporations, and valuations.

- Upward inflection of the purchasing managers index (PMI), which should boost earnings growth.

- Positive investor inflows.

Doesn't this feel like a formula for market strength?

Ebbs and Flows

Let’s keep in mind though, as with any year, market gains won't come without ebbs and flows.

One realistic factor is a “reaction near highs.” The S&P 500* could set new highs in January. If so, some consolidation in the first half of the year is likely. Additionally, historical seasonals in election years show how stocks typically peak in February, then consolidate into April:

Interestingly, that timing would align with the potential for investors getting anxious about interest rate cuts in the first half of the year. As the historical chart shows, there may be a run up through early February followed by some consolidation in the second quarter.

That said, it doesn't mean we or you should be on the sidelines in early 2024. Last year’s strong December implies there will be gains into January and February this year. For example, when December gains are 4.0% or more (like last year), January and February averaged a gain of 2.6% with a win ratio of 73.0%:

Even More Buying in Half the Time

Given that 2024 just started, there isn’t a lot of new data yet. Still, we found an interesting historical comparison to the COVID-19 era run up that’s worth sharing. It’s a near mirror image, though with distinct differences.

Many investors are skeptical of the latest rally. Meanwhile, we've made no secret about being bullish for 2024. Since we love data, let’s see what insights can be gleaned from a side-by-side comparison to the bull run coming out of Covid.

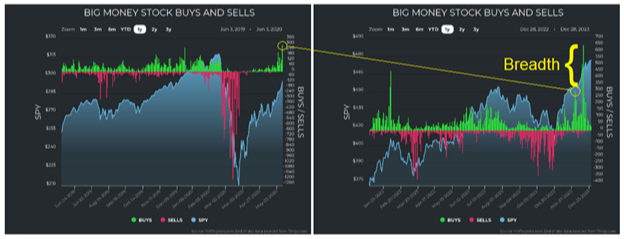

First up, we have the period of June 2019 through June 2020. You may recall how in January 2020 the market was still rising while the BMI started falling. That was the first indication the “big money” was aggressively selling ahead of major global news.

The BMI then went deeply oversold, signaling a significant reversion was ahead. It was – a rally that lasted almost two years leading to a gain of 115.0% in the S&P 500 (chart on left below). Most interestingly, the start of the rally had mountains of money flowing into small- and mid-cap stocks (chart on right below):

Jump to mid-2023 and we see a similar pattern of an overbought BMI falling while the markets remained resilient until the BMI went aggressively oversold. Again, that was a precursor to a massive reversion, which as of this writing has brought a gain of about 16.6% in the S&P 500. Also, there was another series of significant inflows into small- and mid-cap stocks. But this time, there’s been even more buying than in 2020 and it occurred in just half the time:

Now let's compare the annual buying and selling of stocks over these two periods. As you can see, the same pattern of massive buying at the beginning of the rally occurred. It happened on unusual, large-volume, institutional accumulation that was quicker and bigger than in 2020:

These charts paint a picture of investors being on the wrong side of trades and needing to correct quickly. No matter the cause(s), the reality is that buying like this usually kicks off large, sustained moves. In both cases, growth stocks and breadth (unusual buying happening in nearly every market sector) led us higher.

Clearly, the symmetry of these two periods bodes well historically. The rally out of COVID more than doubled the value of the S&P 500. Thus far, the current rally is up “only” about 17.0%.

Admittedly, the key difference this time around is interest rates.

In 2020, governments flooded the world with free money, and we know the undesirable side effect of that was inflation. As a result, interest rates rose to control rising prices.

Now inflation is falling. Yet there's still a significant spread between prices and interest rates:

As the chart shows, since 1960 the federal funds rate is almost always below the consumer price index (inflation). That indicates this inversion will not last much longer.

The Fed already telegraphed six interest rate cuts through 2025. Our base thesis is that the cuts will begin as early as the second quarter this year.

Some may point to Fed Chairman Jerome Powell’s commitment to 2.0% inflation over time. However, since 1960 the average rate of inflation is almost 3.8%. So, 2.0% inflation is a unicorn, though it’s nice to have goals.

Additionally, the average federal funds rate since 1960 has been almost 4.8%, though it's been much lower recently. Since 2000, the federal funds rate averaged about 1.8% while inflation has averaged about 2.6% (which is still greater than Powell’s unicorn).

In short, what we mean is that rates will fall, leading us to have conviction that there could be a long bull run for stocks with interest rates as a strong tailwind. It would be like the COVID period, but with a twist. This time there are higher interest rates, but stocks rallied anyway. They could gain more as those rates decline to a more sustainable long term norm, just like during the COVID rally.

Also, let’s not forget the record $6 trillion in money market accounts. Falling interest rates and yields will have that cash seeking higher returns. We know interest rate moves up or down are catalysts for market performance. We think 2024 will prove that case again.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

*Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.