Few pundits could’ve imagined the rally we're currently experiencing. For a long time, the doomsday narrative was everywhere you turned. However, our readers know that we saw brighter days ahead through our data-based approach.

As we sit here today, that approach still signals a bullish forecast. After all, it isn't often that the S&P 500* surges more 16.0% in 36 trading days.

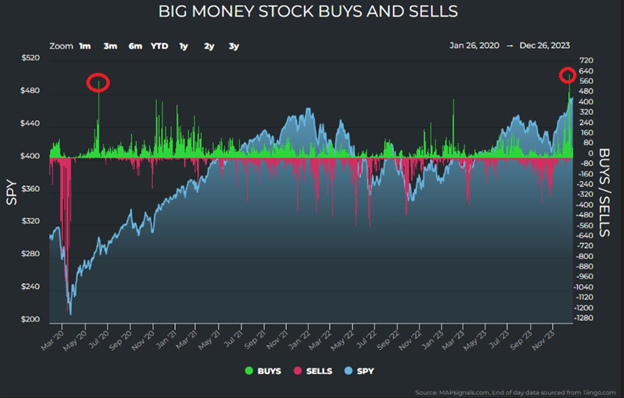

Still, it’s important to note how deep the depths were just weeks earlier. Small-cap stock valuations were at historic lows and MAPsignals’ trusted Big Money Index (BMI), a 25-day moving average of stock buys and sells from “big money” professional investors, hit its shallowest readings since the pandemic.

But we’ve seen time and again that when the market’s “pendulum swings” are violent to one side, the correction is just as powerful in the opposite direction. Hence the phrase, “The bigger the dip, the bigger the rip.” We believe that this recent “equity ripper” is partly due to the severity of the September and October selloff.

While the current rate of momentum is unsustainable, there’s historical evidence that paints a positive picture moving forward. Today we’ll explore some charts to show how powerful this latest move is and what may possibly lie ahead based on historical precedent.

Most Powerful Inflows

The Federal Reserve’s latest report from its survey of consumer finances shows more American households own stock than ever before. These huge levels of participation mirror the push of the BMI to heights not seen since the pandemic. The latest reading of 89.3% is rarely breached:

Only the most powerful inflows can push the BMI to such extremes. If we dive below the surface, we can identify why the BMI is currently popping off the chart. On Dec. 14, the largest inflow day ever in MAPsignals’ data was recorded. A mind-blowing 650 stocks were accumulated that day, even more than the previous biggest day (June 5, 2020, when 597 equities were bought):

When 40% of the equity universe logs green buy signals like this, it indicates all sectors are participating in a broad rally. These rapid rises are common after equity wipeouts, showing the “market pendulum” does truly swing back at some point. The current “swing back” began in late October after the BMI bottom, which is when we began to pound the bullish drums.

There have been plenty of past oversold markets to analyze. So, we shouldn’t be surprised as stocks surge out of these oversold conditions. This happens in markets, and it will happen again.

This time was no different, except for one major aspect – the Fed pivot was telegraphed. This allowed an already heated market to be sent into overdrive. With the Fed now set to cut interest rates, the macroeconomic outlook provides a powerful tailwind for additional equities support into 2024.

Soaring Breadth, Participation

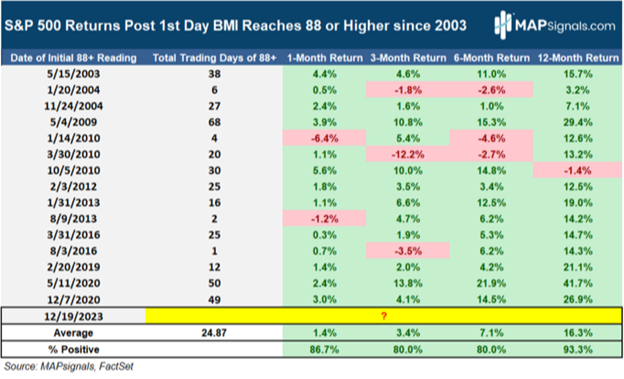

Normally the BMI reaching overbought levels (80.0% or more) is a signal for near-term bearishness. But in rare instances, readings of 88.0% or more do occur. We’re in one now. Our friends at MAPsignals went back and studied every day when the BMI breached 88.0% and the findings are stunning.

Since 2003, there have been 15 periods where this condition is met. Interestingly, once the BMI breaks into this ultra-high area, it tends to hang there for an average of 25 trading days. Possibly more impressive are the returns for the S&P 500 going forward from the first day the BMI pierces 88.0%. On average, a month later stocks are up 1.4%, three months later they’re up 3.4%, and after a year they’re up 16.3%:

Using the same framework, the S&P Small Cap 600 universe crushes the S&P 500. This is because in order to reach a BMI of this magnitude the rally must be broad enough to reach not just large cap stocks but small cap equities as well. After the BMI eclipses 88.0%, on average small-cap stocks gain 5.8% after three months, 10.4% after six months, and 22.1% after a year:

To us, this historical study suggests we're just entering a period favoring heavy equity appreciation. More support exists when examining forward-looking price-earnings ratios from a valuation standpoint. The popular “too expensive” narrative is debunked because, as of this writing, valuations are still attractive:

If that’s not enough, we saved the hammer from MAPsignals for last.

There are plenty of ways to slice the data, but the recent stock surge created some of the highest readings of buying relative to selling ever. What does that mean?

As an example, a day where 90 stocks were bought and 10 stocks were sold gives us a 90.0% buy day. That same 90% ratio can occur with 450 stocks bought and 50 stocks sold. Obviously, the latter has a much higher participation rate, which gives more weight to breadth of stock performance.

MAPsignals normalized the recent buying relative to selling, rather than just using a simple daily moving average. This exercise showed that 3,986 stocks were accumulated in the last five weeks, while only 362 were sold. Contrast that to the last time the BMI went overbought, when 2,490 stocks were bought and 468 stocks were sold.

This time around, there’s a 60% higher participation rate. That is significant from a magnitude of accumulation standpoint. Normalizing this level of relative buying reveals a 91.6% breadth rate, which is extraordinarily rare. It provides data-backed evidence that the pundits proclaiming this rally doesn't have legs don't know what they're talking about.

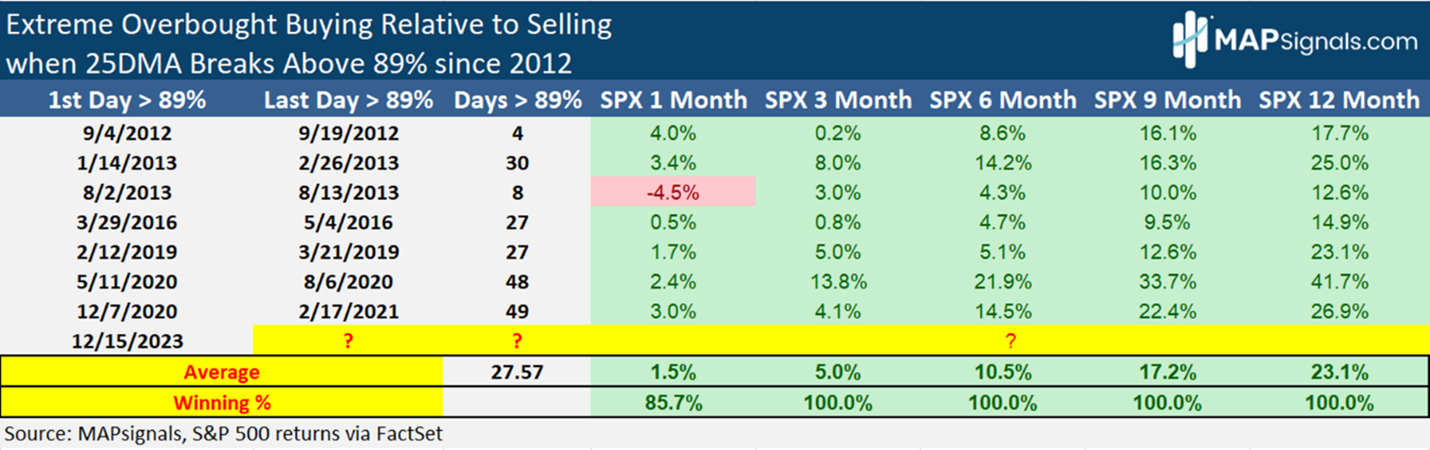

If we look back to 2012, there have been only seven instances of participation rates greater than 89.0%. The S&P 500 has never been lower three-to-12 months out in those occurrences, and after a year, stocks rose 23.1% on average:

If you can combine all this with The 12 Charts of Christmas, it seems foolish to fight the data and not continue to expect a continuation of this surge in the near term.

*Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.