Over the past few weeks, unsurprisingly, the mainstream media headlines have spent their time espousing worry about the wrong things specifically in regards to equity markets. There are multiple examples easily found with an online search, including U.S./Iran deals being rejected, uranium concerns, “climbing” inflation expectations, and broad concerns around the task in front of the new Federal Reserve Chair, etc., etc., etc.

Initially, the S&P 500 reacted with some volatility air pockets. It caused the index to tick off recent peaks before subsequently getting its emotions back under control and rebounding to new record highs through the end of last week:

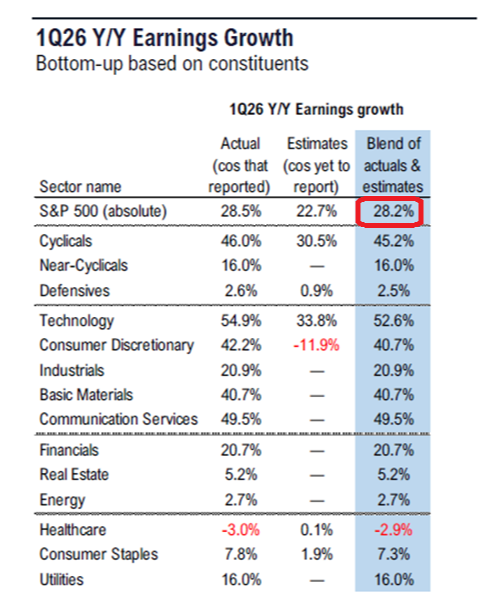

The market began to regain its composure as FactSet released its first-quarter earnings recap. Our readers know the results broke records. The blended earnings growth rate is an astounding 28.2%:

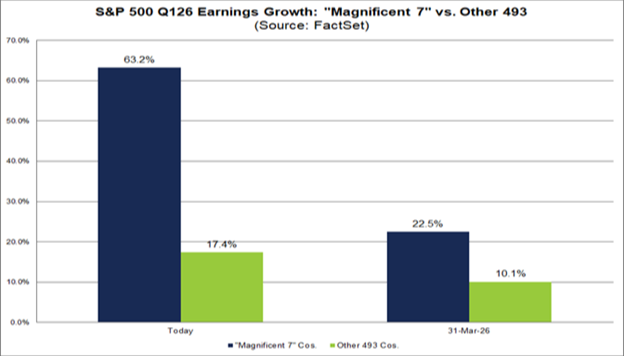

The FactSet recap provided additional phenomenal data when looking just below the surface. For instance, net profit margins hit 14.8%, the highest level going back to 2009. Also, the most important growth drivers in the market, the Magnificent 7, grew earnings by over 63%:

That number on its own is ridiculous, but it’s even more impressive knowing that on March 31 the estimated earnings growth rate for the Mag 7 was expected to be a “mere” 22.5%.

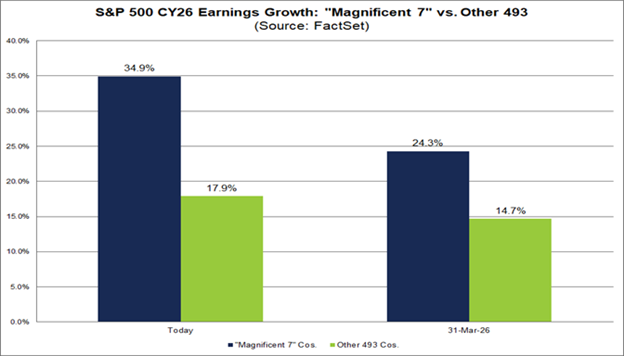

The magnitude of this earnings surprise also significantly impacted the calendar year 2026 estimated earnings growth rate for both the Mag 7 and the rest of the S&P 500. Heading into earnings season, the Mag 7 estimate for calendar year earnings growth was 24.3%. It’s now up to 34.9% as we close out this earnings season:

Perhaps we at Cornerstone are beating a dead horse. But we point out the extraordinary results of this earnings season once again to firmly illustrate the disconnect between headlines and data. Headlines say the current rally is overextended while earnings show corporate America just delivered one of its strongest historical quarters, further cementing the fundamental underlying strength of these companies.

Headlines have been screaming fear. But the fundamental data story is much brighter, and most importantly, it’s supported by institutional money flows.

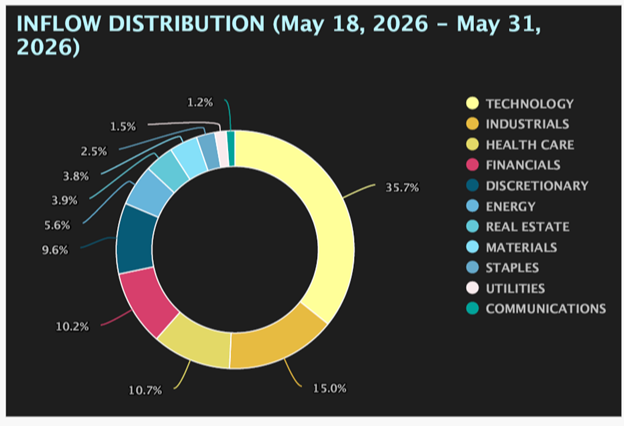

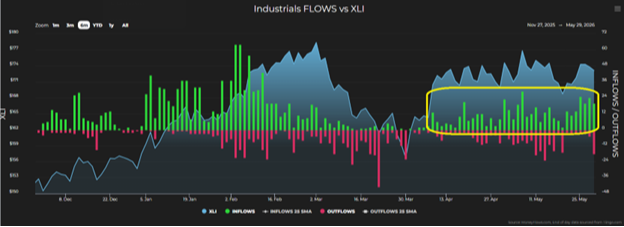

There have been clear surgical leadership winners, continuing this quarter's thematic rotation and reallocation of capital. In fact, the technology and industrial sectors alone accounted for 50.7% of all inflows over the last two weeks:

The repeated, consistent strength in industrial inflows since early April continues to indicate that capital allocation is not slowing into the companies that are the key supporters of the AI build-out infrastructure and hard asset trade:

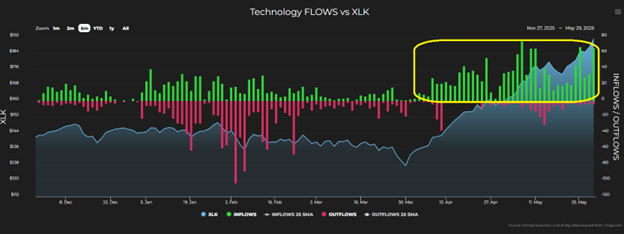

Additionally, the technology sector continued to rip as it has throughout the second quarter:

However, from a thematic positioning standpoint, leadership within technology continues to narrow. Specifically, buying is consolidated in networking, semiconductors, and AI security.

Clearly the market isn’t buying technology as an entire sector anymore. Rather, institutional investors are laser focused on buying the hardware and infrastructure layers while selling the implementation layer (i.e., software).

To be clear, this is a regime-defining distinction.

In our opinion, this is an indication that the market isn’t in euphoria mode, but instead carefully conducting surgery. Capital flows are targeting with a single question: does this company benefit from the construction of the new industrial economy?

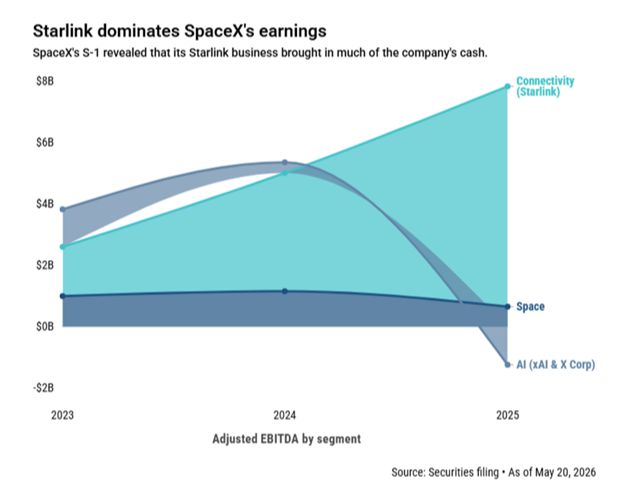

This narrowly focused capital deployment theme is further exemplified by the expected record setting initial public offering for SpaceX. This is not merely a rocket company that is going public. It’s the consolidation of launch, satellite communications, data, compute, and internet infrastructure all wrapped under a single corporate umbrella.

This company is an explicit thesis proving out that the next industrial layer of civilization will be built in low-Earth orbit and beyond. Hence, “big money” capital is rushing to gobble up SpaceX shares not because it can shoot a rocket into space, but because underneath the surface it’s a pick-and-shovel play for the forthcoming orbital economy. This includes power, materials, communications, autonomy, and robotics.

For those not paying attention, the flow data has been pointing in this direction while the headlines have not yet caught up. When you analyze the actual data and pull the threads together, a single story emerges.

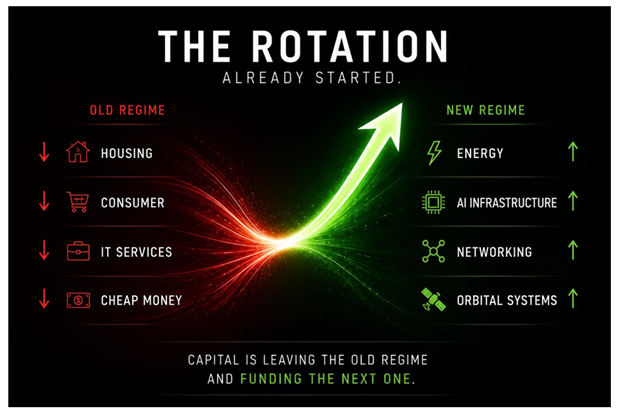

That is, the market is doing what markets always do at the start of a regime change: rotate. Investors are selling the old regime and redeploying capital into the new one.

Flows show what’s being sold is housing dependent on cheap mortgages, consumer cyclicals dependent on stretched households, speculative materials, IT services dependent on cheap labor arbitrage, and over-regulated utilities priced for declining rates.

Conversely, the new regime being bought includes:

- Energy that powers AI

- Networking that connects it

- Semiconductors that compute it

- Financials that finance the build-out

- Real estate that houses the data center racks

- The orbital stack that will host the next generation of data centers entirely

For most investors, the fact that the S&P 500 is hitting new highs masks how surgical this rotation is underneath the surface. On the macro index level, everything looks normal. But from an underlying data standpoint, we recognize an enormous reallocation is happening.

In our opinion, the SpaceX filing and upcoming IPO very well may be the inflection moment that Wall Street and the headlines will be forced to model this new regime appropriately.

As always, the market positioned itself early as the headlines looked the other way. This is another clear example of the importance of being consistent with our strategy and having conviction in our thematic underpinnings within the market.

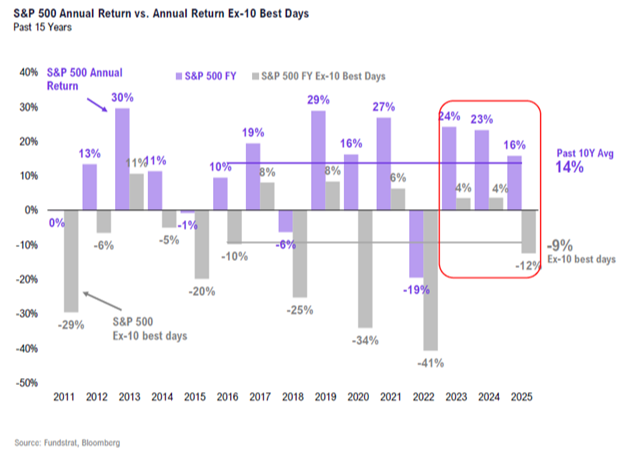

Headlines and Black Swan events will always create bumps. But if we allow fear to steer us off course and try to time the ups and downs, historical data will show us that’s a fool’s errand.

As a reminder of that reality, let’s revisit a CFS favorite illustrating the difference in annual returns if you missed merely the 10 best days each year:

If you try to time the market, there’s a good chance you’ll miss one or all of the year’s 10 best days. And clearly that is not good for wealth creation.

Instead, consistent long-term conviction grounded in objective data allows the flows to show us exactly where the future has first arrived.

(The full clip for those interested)

*Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

*Past performance does not guarantee future results.

*Investing involves risk and you may incur a profit or loss regardless of strategy selected.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.