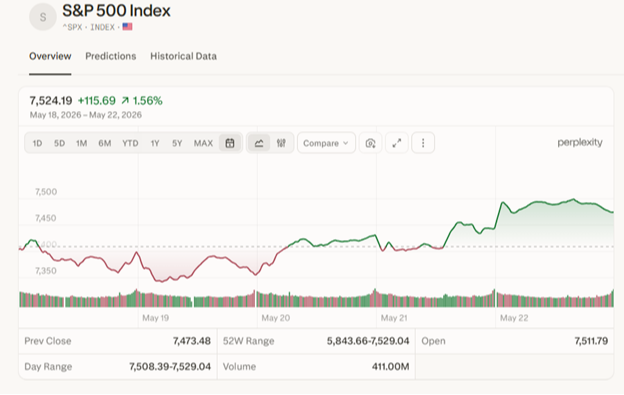

As earnings season ends and we enter a slow data period, equity markets began to pause, and news headlines got louder in the absence of new fundamental objective data. As such, the S&P 500 was essentially flat last week until closing with a strong Friday:

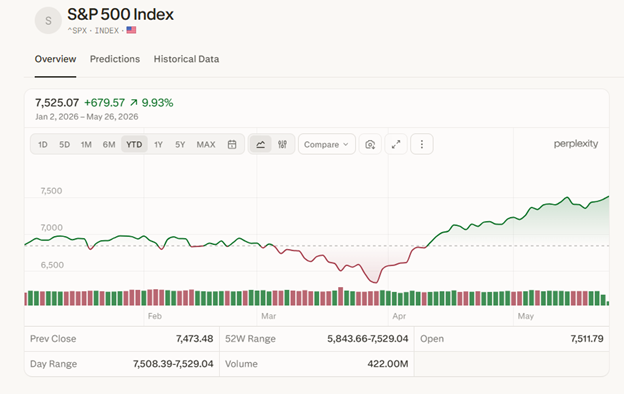

But at Cornerstone we think it’s a sign of impressive resilience in the face of emotionally driven headline narratives. This resilience is further reflected in surprisingly strong year-to-date performance:

This is especially impressive considering markets are still facing big headwinds like oil being near multi-decade highs:

And the current interest rate environment being at one-year highs:

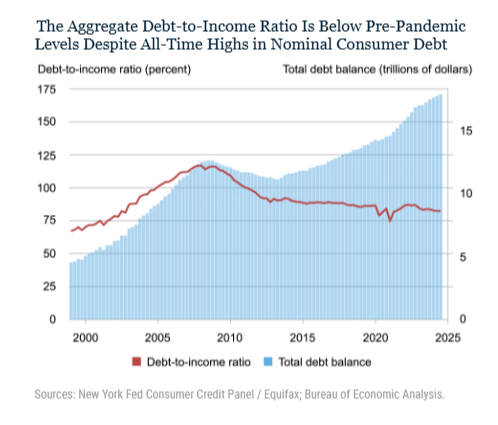

In our opinion, this resilience reflects the fact that investors are embracing the current strong fundamentals fueled by AI spending and the relative energy surplus we have in the face of high oil prices. Also, contrary to the popular narrative, there seems to be a resilient consumer base with relatively low debt. It’s reflected in the consumer debt-to-income ratio, which has dropped to below pre-pandemic levels:

That said, in the short and intermediate terms, we’ll monitor the delicate balancing act incoming Federal Reserve Chair Kevin Warsh must navigate to avoid criticism from the White House. As reflected in the recent minutes, there’s increasing concern at the Fed regarding headwinds pushing against inflation stability and employment stability:

From a macro perspective, we still expect an increase in volatility and slight pullback throughout the summer and early fall months due to midterm election uncertainty. Still, our optimism throughout the remainder of the year remains high.

That was reinforced last week when NVIDIA, the most important company within the S&P 500, reported blowout earnings. Its revenues grew 85% year-over-year, and it had a gross margin of 75%.

For a company that size to grow 85% is astounding. More importantly, the trade isn’t overextended. Even with the stock’s multi-year run, the current valuation is less than half of consumer staples companies like Costco and Walmart:

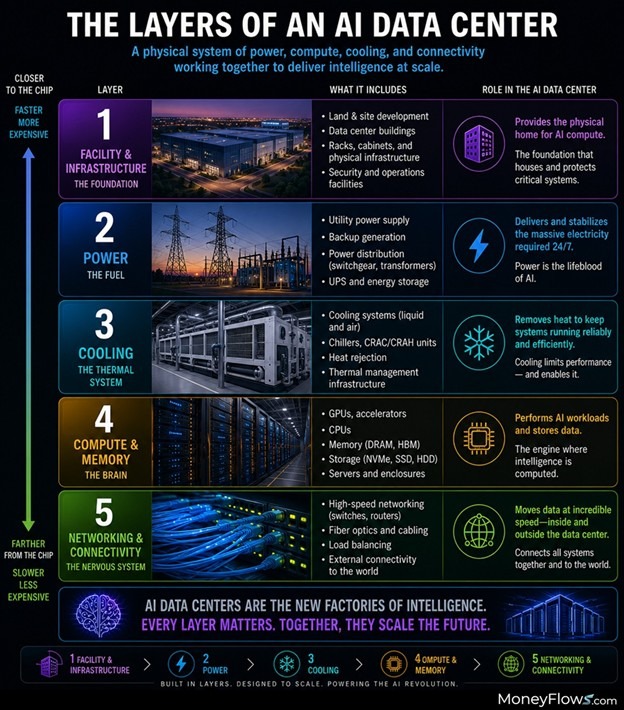

What’s more, the details from NVDIA’s earnings further reinforce the current AI infrastructure multi-year opportunity. Traditional sector allocations are breaking down in favor of thematic capital deployment.

Specifically, capital is chasing five specific layers within data centers:

Even in the face of mainstream headline narratives, NVIDIA’s beat and raise solidified a continuing AI trade. The company now has an almost $5.5 trillion market capitalization with no clear end in sight.

For perspective on the market resilience, let’s remember a handful of “major event” headlines that began to rear their ugly heads once again over the last week as earnings season wound down. Headlines like these:

- Inflation accelerated to 3.8%.

- Wholesale prices ran even hotter at 6% annualized, the worst reading in nearly four years.

- Real wages turned negative for the first time in three years.

- Public consternation and back-and-forth leading up to and into Chair Warsh’s confirmation, which came with the narrowest margin in history.

- Brent crude oil prices remain elevated as the Strait of Hormuz is effectively shut while daily conflicting narratives spout from Iran and the White House.

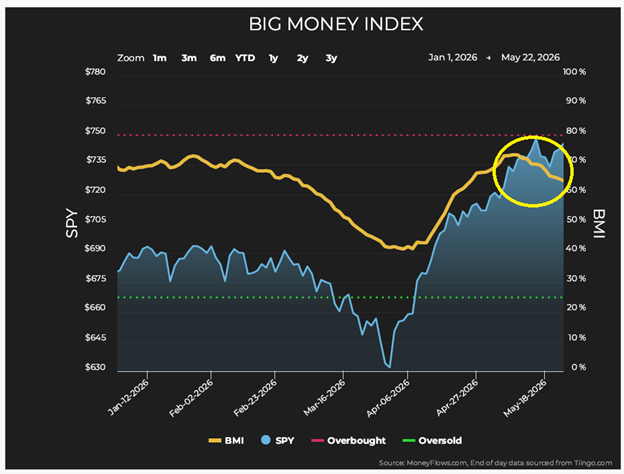

If you read those headlines in any order, you’d think it should’ve been a risk-off week with elevated volatility, just like we saw throughout Q1. But as headlines screamed danger, the all-important long-term money flow trend also stayed resilient:

Perhaps more importantly, headline narratives didn’t spike volatility as the CBOE Volatility Index (VIX) – the market’s fear gauge – stayed under 18, which is wholly different than last quarter:

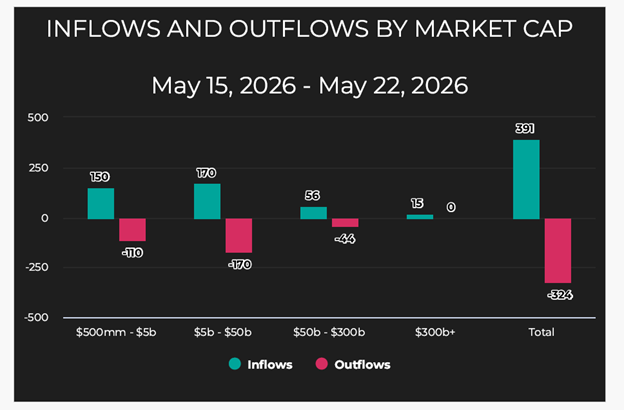

These are clear, effective data signals that the current pause isn’t a material break due to underlying market conditions. If that was the case, we wouldn’t have still experienced more buys than sells over the last week:

We continue to see the AI infrastructure complex attracting capital. Additionally, an important signal became clear last week showing the current overall strength of the equity capital markets via a flurry of initial public offering news.

First is Cerabras Systems (CBRS) going public in the largest U.S. technology IPO since Uber. The deal was reportedly 20 times oversubscribed and opened at almost $350 a share compared to the expected price range of $185.

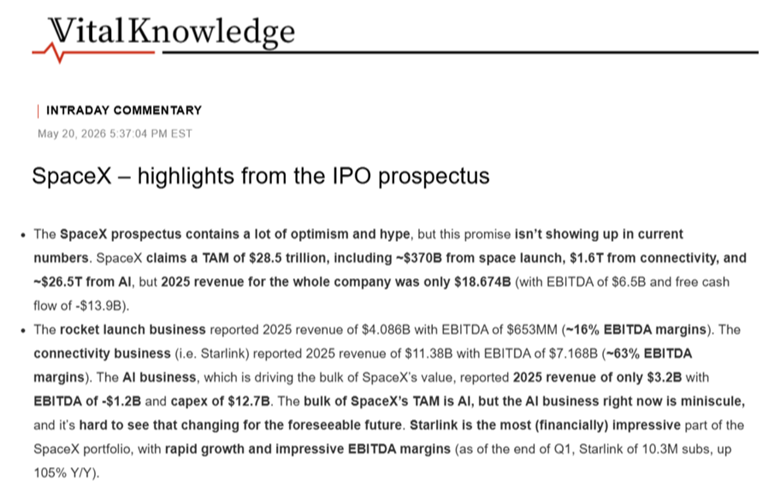

Also, SpaceX released its preliminary prospectus with the most astounding data point being that the expected pre-money valuation would be around 2.7% of the total U.S. equity market. That would be the largest IPO ever.

Then OpenAI’s IPO plans became public knowledge, which could rival the scale of SpaceX:

These are clear examples of the desire for institutions desire to continue deploying capital. It’s not how risk-off markets behave. When there’s a divergence from the popular bearish narrative as the smart money continues to buy, it usually means institutions see something headlines haven’t caught up to yet.

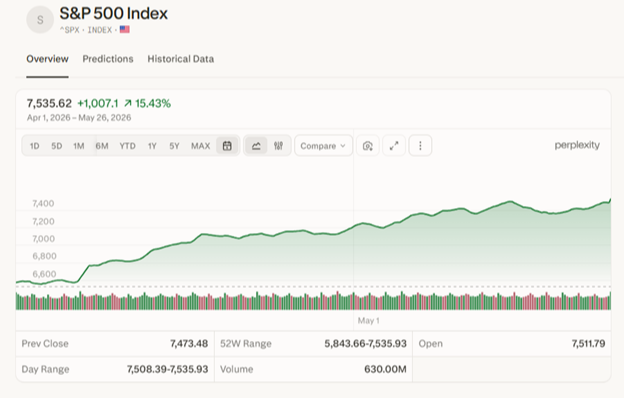

As we've been discussing for weeks, the “big money” capital is continuing to position itself strategically. These deployments have been the driving force behind the S&P 500’s 15.43% rocket growth since April 1:

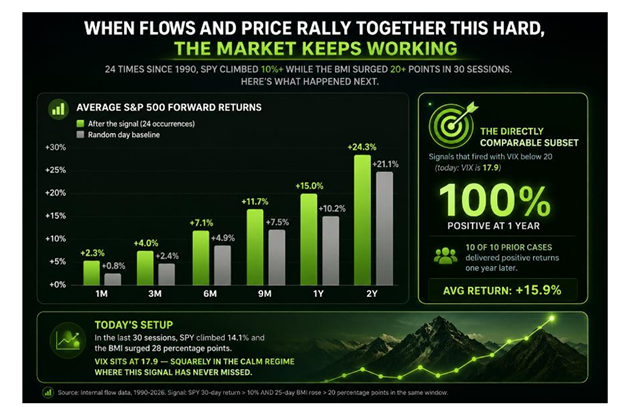

In similar setups since 1990, there have been 10 instances when money flows and market prices rallied together this significantly with the VIX below 20. In all 10 instances, stocks outperformed baseline averages:

In this setup, the average gain a year later is 15.9%.

The current underlying fundamental data and money flow trends show investors are buying with conviction into a calm market that just absorbed the hottest inflation print in three years without breaking. That matters.

Obviously, markets can be irrational, especially in the face of uncertainty. As we’ve said all year, that will not be unexpected as we enter the always-entertaining midterm election campaigning season.

But let’s be clear: short-term uncertainty is not a material macro event that would overwhelm the current fundamental strength of the market over the long term. For us at CFS, potential risks that would have a real negative long-term effect on stocks would be a visible deterioration in the consumer, widening credit spreads, or a sharp spike in the VIX of over 25 for an extended period. Those are the data points we will be keeping a close eye on.

The headlines are trying to say the markets are fragile due to world geopolitics. But the data and flows show us which trades should continue to thrive, even in the face of those headlines.

*Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

*Past performance does not guarantee future results.

*Investing involves risk and you may incur a profit or loss regardless of strategy selected.

#NVDA is owned in CFS client accounts and by Daniel Milan personally.

#CRBS is not owned by CFS clients or Daniel Milan.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.