Daniel J. Milan, JD

Putting a bow on this earning season, today we’ll review the historically staggering first-quarter results. In doing so, we’ll show how these earnings results are not just a blip on the radar.

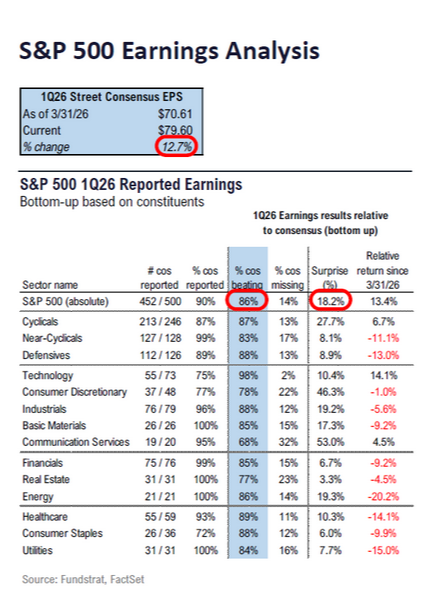

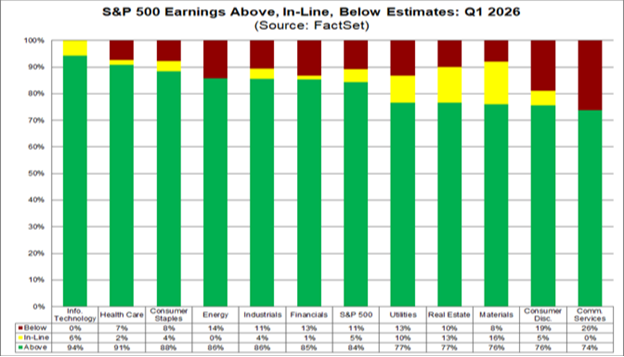

As of this writing, 90% of S&P 500 companies reported earnings results. Both the number of positive earnings surprises and the magnitude of those surprises are well above recent averages.

For instance, 86% of firms have reported actual per-share earnings above estimates. That’s significantly above the five- and 10-year averages of 78% and 76%, respectively.

More astonishing, in aggregate these companies are reporting earnings that are 18.2% above estimates.

That blows away the five- and 10-year averages of 7.3% and 7.1%, respectively, and surpasses even the most bullish expectations at the end of March.

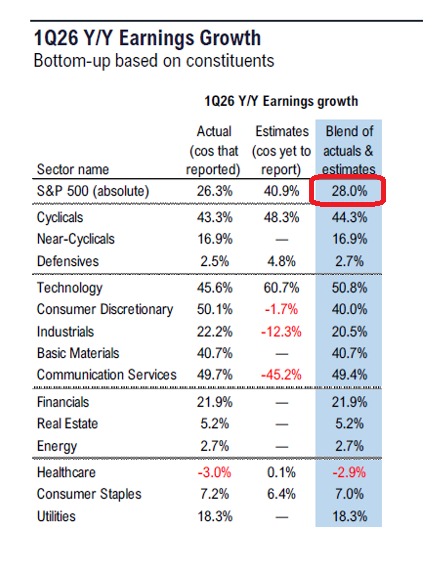

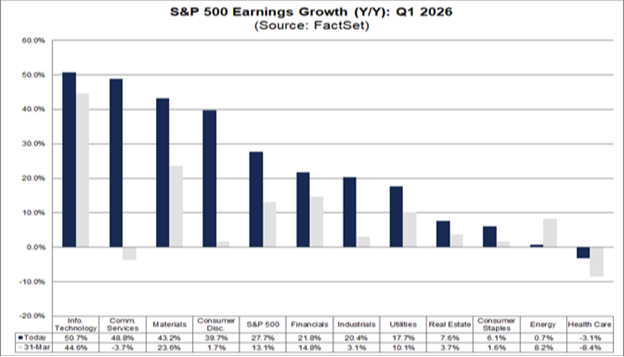

Even more revealing is the almost unbelievable earnings growth rate. Currently, the blended earnings growth rate for Q1 sits at 28% year-over-year:

That’s more than double the initial projection of 13.1% on March 31.

And the best part is the growth is broad – 10 of the 11 market sectors are reporting year-over-year earnings growth, and seven are reporting double-digit earnings growth:

Looking forward, these record-setting numbers allowed analysts to increase their growth rate projections for the remainder of the year. Today, analyst EPS growth expectations for the remaining quarters are 19.9%, 23.2%, and 20.7%, respectively.

If that occurs, the 2026 year-over-year earnings growth rate would be 21%. In Cornerstone’s opinion, current data indicates 21% would be at the low end of what’s possible.

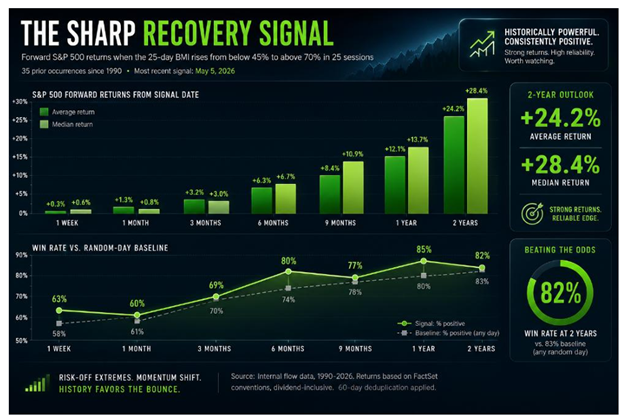

To lay out the support case, let's rewind to six weeks ago. Fear was at its peak as MoneyFlows’ trusty Big Money Index (BMI) cratered to almost 40%. Since then, the BMI jumped over 38 points in only 28 trading sessions:

This extreme reversal indicates a full, earnings-based regime change. To understand the importance, our friends at MoneyFlows studied similarly sharp recovery signals from history (when the BMI rose from below 45% to above 70% in a 25-day window):

It’s happened 35 times since 1990, producing solid forward returns:

- Six months later, positive 80% of the time with a median return of 6.7%

- Nine months later, positive 77% of the time with a median return of 10.9%

- A year later, positive 85% of the time with a median return of 13.7%

- Two years later, positive 82% of the time with a median return of 28.4%

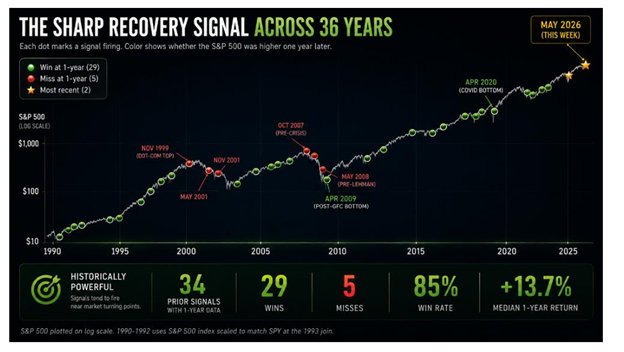

What’s also interesting is what happened in the five misses within the data. Over multiple decades, those five misses cluster in two obvious places:

First was the 1999 dot-com bubble through the early 2000s recession. Next was the years leading up to the Great Financial Crisis. Importantly, each of these involved a macro shock.

When the macro environment holds firm, the signal works 100% of the time. But if the macro environment breaks, nothing works.

This keeps us alert for any potential macro risks that could derail this trend.

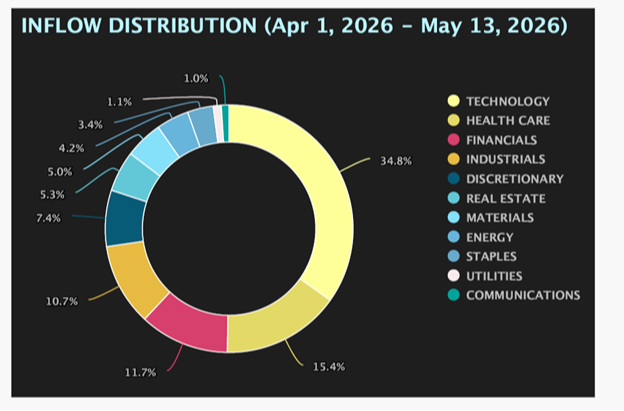

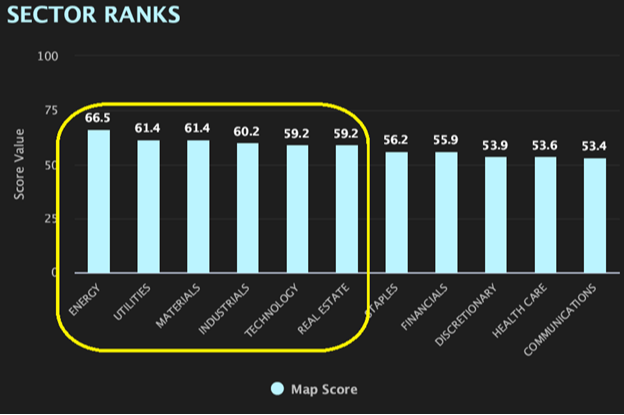

Going further, this bullishness has staying power due to what’s being bought. This isn’t panic buying; it’s institutions repositioning entire portfolios.

Since April there’s been broad buying across the most important growth sectors:

Furthermore, combining fundamental and technical data, the strongest sectors are supporting the AI infrastructure boom and driving record earnings growth:

This shouldn't be a surprise. We all know the importance that energy and utilities are playing to meet AI data center demands.

Energy: Natural Gas

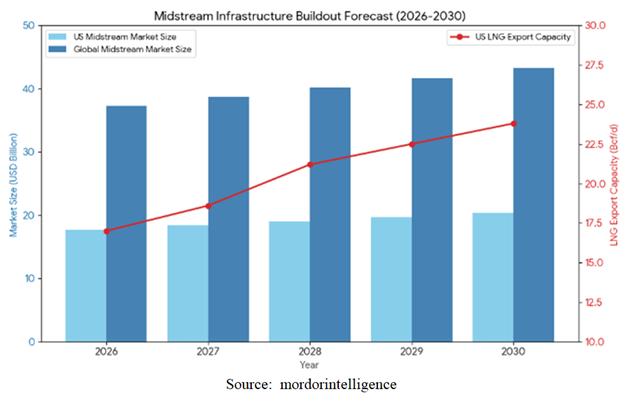

So far, the natural gas energy sector is the biggest beneficiary in terms of future energy demand. Impressively, over the next five years, demand for midstream infrastructure is entering what analysts are calling the biggest build-out surge in 20 years. The market is projected to grow from $77.6 billion in 2026 to $92.6 billion in 2031.

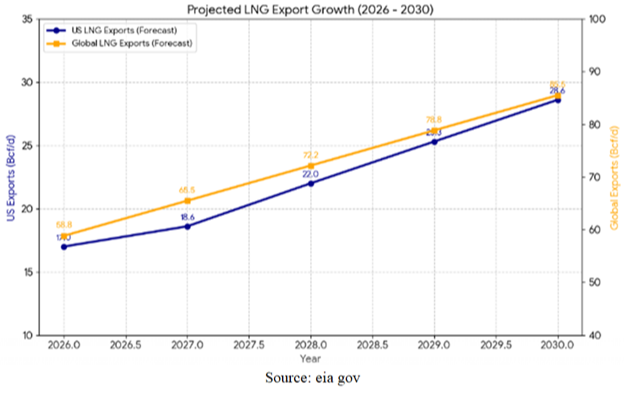

Even better, the biggest driver for new pipeline terminal capacity is domestic. American export capacity is on track to rise 80% by 2028 and actual natural gas exports to rise 30% by 2027 alone, reaching over 20 billion cubic feet per day.

Major AI facilities consume up to 500 megawatts of continuous power. So, natural gas midstream operators are in demand. Analysts expect data center demand alone to drive natural gas consumption up by 3.3 billion cubic feet per day by 2030.

The biggest and the best natural gas companies are able and willing to accommodate this growth. Two are some of our favorite dividend growth companies.

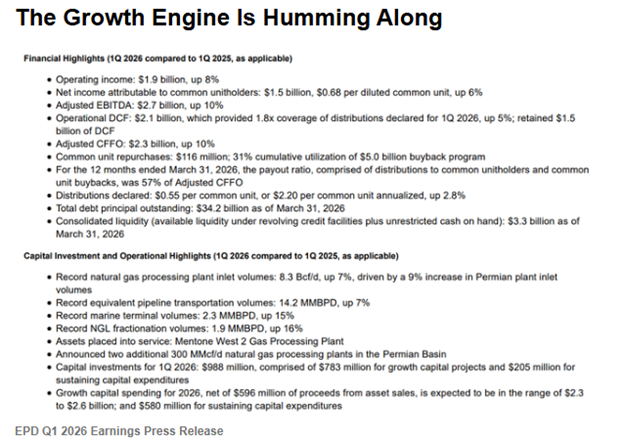

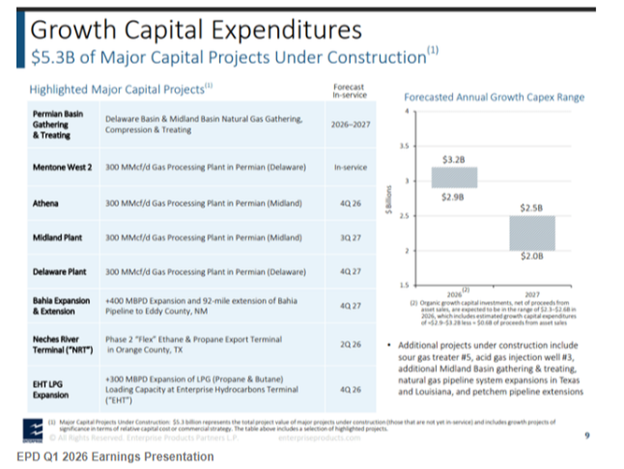

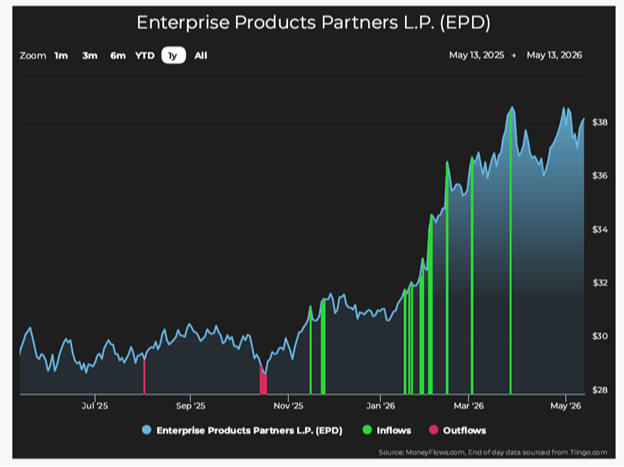

The first is Enterprise Product Partners (EPD). Its recent earnings call showed record revenue growth and huge capital investments.

Furthermore, institutional inflows have persisted all year:

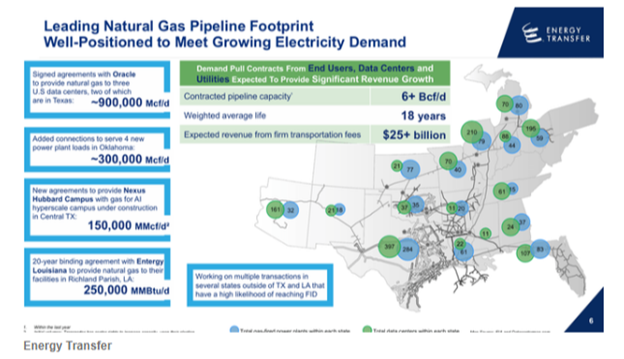

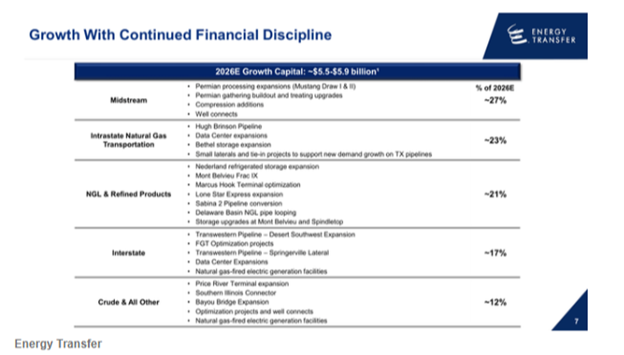

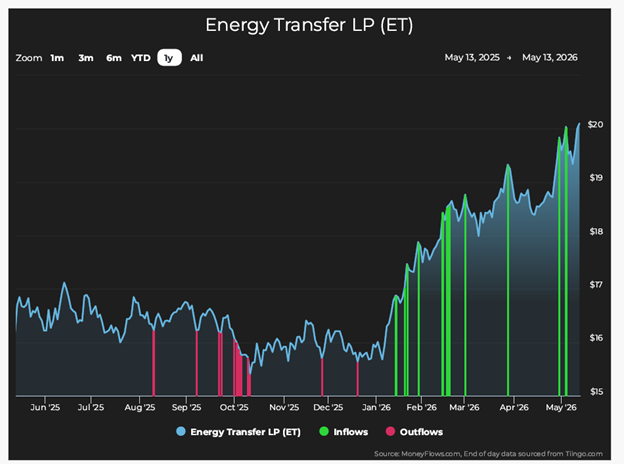

We saw the same supportive growth data from Energy Transfer (ET) in terms of revenue and capital investments:

Not surprisingly, the institutional money inflows have been accumulating:

The growing number of data centers needs energy to run. Natural gas will be one form of it.

Technology – Data Center Suppliers

Let’s now look at examples of companies providing the core needs of custom chips, networking, and connectivity to support data centers.

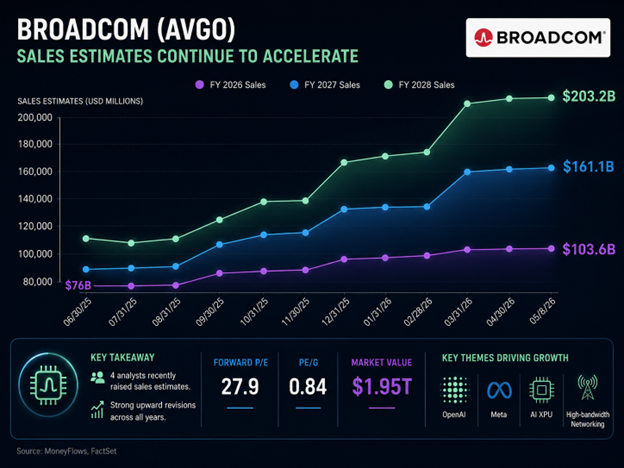

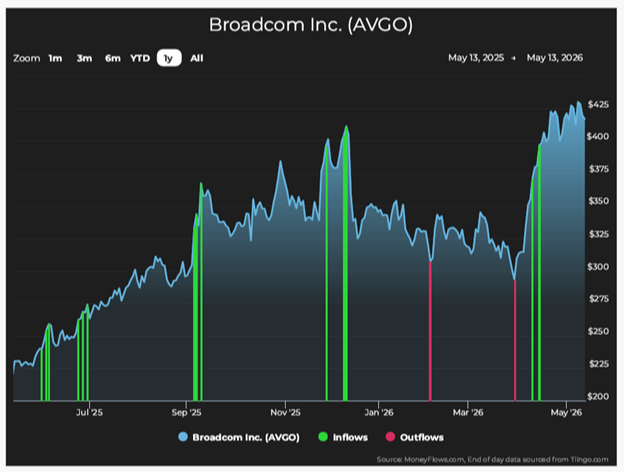

Broadcom (AVGO) provides high-performance switches and connectivity solutions. While many have been behind the company for a while, we think Broadcom’s rise is just beginning.

The company’s annual sales estimates are projected to double from $103.6 billion in 2026 to $203.2 billion by 2028:

This growth is why institutions have been piling in to the stock with no indication of stopping soon:

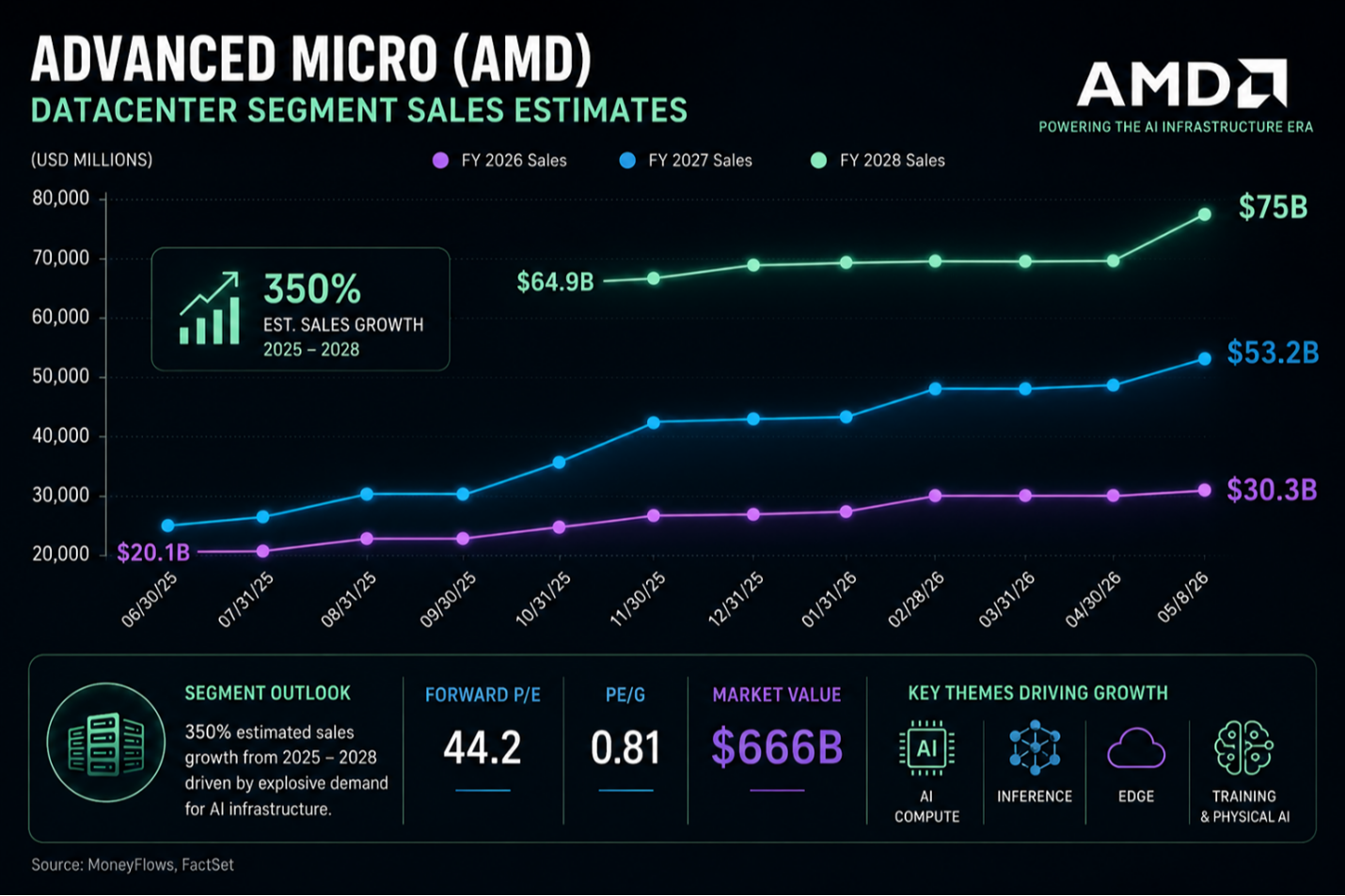

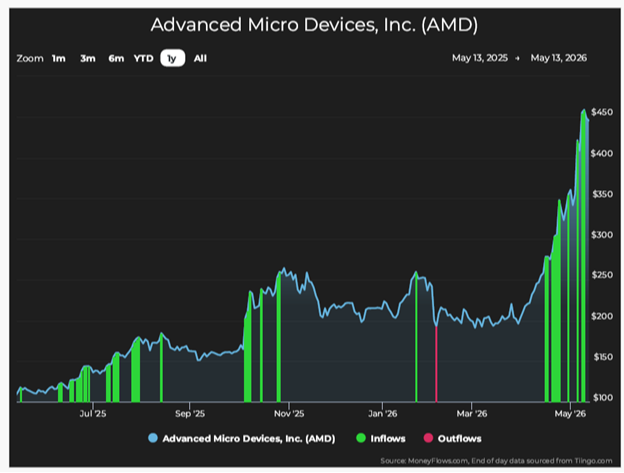

Another great revenue story is Advanced Micro Devices (AMD). It’s a giant for the inference and physical AI necessary within data centers.

AMD's expected data center segment sales growth is staggering:

This segment is expected to rise from $30.3 billion in 2026 to $75 billion in 2028.

Once again, explosive sales growth attracts institutional capital at scale:

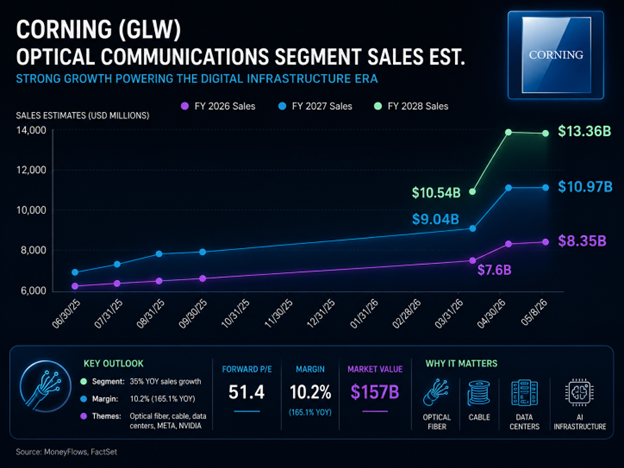

If these projections aren't enough, here’s one more. It’s also been our favorite stock for over a year – Corning (GLW). AI data centers rely on connectivity speed solutions and Corning is a leader in optical connectivity solutions for AI infrastructure.

Its optical communications segment is expected to increase sales from $8.35 billion in 2026 to $13.36 billion in 2028:

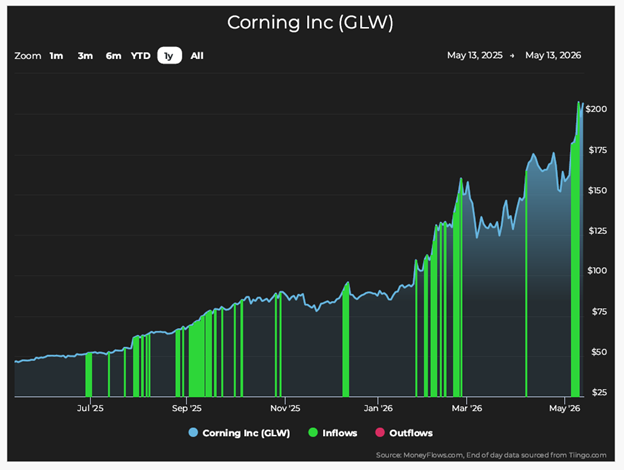

Once again, this growth brings massive institutional inflows:

A year ago, GLW traded at $51 per share. Big Money is still paying over $200 a share now.

Taken together, this data shows a durable advance. Capital isn’t buying indiscriminately. This tape and this market deserve respect.

* Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

*Past performance does not guarantee future results.

*Investing involves risk and you may incur a profit or loss regardless of strategy selected.

^EPD, ET, AVGO, AMD, and GLW are owned in Cornerstone client accounts

*EPD and AVGO are owned by Daniel Milan personally

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.