There was wobbly action in equities markets last week with up-and-down reactions to the news of the day. Monday and Tuesday were down, while stocks recovered on Wednesday and Thursday. Naturally, with the early-week declines came habitual proclamations of this bull market being finished. We’ve heard that before in 2024. But in past cases and last week, the dips were bought, and markets stabilized.

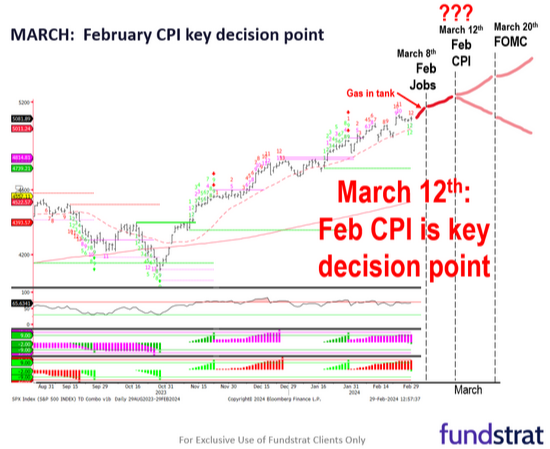

From a technical standpoint, the key level we are watching on the S&P 500* is 5,057. If the index falls below this point, it will signal the possibility of a short-term, multi-day decline:

But overall, the technical picture remains positive. There may still be some gas left in the tank. That said, two important considerations remain.

First, last week we saw days with both decreased bond yields and equity declines. This is a somewhat significant change in character as stocks have typically gone up on days when yields fell during this bull market run:

The next concern is a combination package. It includes Federal Reserve Chair Jerome Powell’s commentary last week, along with fresh jobs data, and the upcoming February consumer price index report due out this week.

The bottom line is that this is an extremely mature rally. As of this writing, we're 19 weeks in with a cumulative S&P 500 gain of around 26.0%. This duration is now longer than the two previous rallies that occurred since October 2022. The first one lasted 16 weeks (October 2022 – March 2023) while the second lasted 19 weeks (April 2023 – October 2023).

There are solid fundamental arguments for this rally to continue. There’s the doveish turn by the Fed, expected interest rate cuts, and continuing recession risks abating. These all point to stock gains ahead. Still, there are potentially key catalysts, both good and bad, that we’ll be monitoring closely in the next couple weeks.

Planning and Pivoting

Here’s a reminder to our readers (and ourselves): absent a plan, you plan to fail. Think about how we plan our lives based upon common assumptions. For instance, we assume there won’t be disruptions to our modern ways of life. So, we plan for what we think will happen.

Despite best efforts and intentions, people often don’t plan for unexpected things that can disrupt the way we live. The possibility that you wake up tomorrow and everything is broken is largely discounted.

But we all know how life throws curve balls sometimes.

Just a few weeks ago a vast cellular network outage made it so many folks couldn’t place a call, send a text, or browse the internet. They couldn’t even dial 911 in case of an emergency.

At CFS, we plan for the unknown as best we can. To do so, we attempt to stack the odds in our favor.

The heart of those efforts is our longstanding commitment to a data-driven approach. We supplement that with nimbleness – a mindset that we’re ready to act if environments change.

What does that mean for the current landscape?

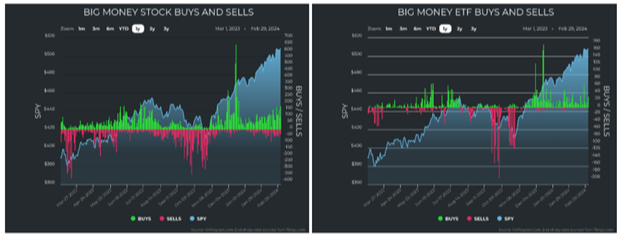

From a planning perspective, the trusty Big Money Index (BMI), which is a 25-day moving average of “big money” investor stock buys and sells from our friends at MAPsignals, fell from overbought territory in early February:

Historically, that would indicate a near-term market drop and that we should be ready to scale back on risk. But that hasn’t happened…not yet anyway.

So, we must be ready to pursue an alternative course. That can even mean staying put, which is why we’ve been saying we’ll remain steady until the data shifts.

This may seem counterintuitive. After all, isn’t the BMI falling from overbought a shift in the data? Well, like many things in life, it depends.

Peeling back the layers, we can see the BMI has fallen due to a decrease in extreme buying activity, not an increase in selling activity. That’s an important distinction. Buying is still healthy, it’s just not at the levels we saw in December 2023:

If selling hasn't picked up and stock prices keep rising (like what's going on now), it historically indicates a pause in underlying market strength. But it does not imply weakness.

There’s further support for this idea in the fact that markets keep rising on the back of steady, unusual volumes. The only thing that fell was the extreme heavy buying in December. What would capture our attention is heavy selling materializing along with a falling BMI, as it would be a significant change in the data.

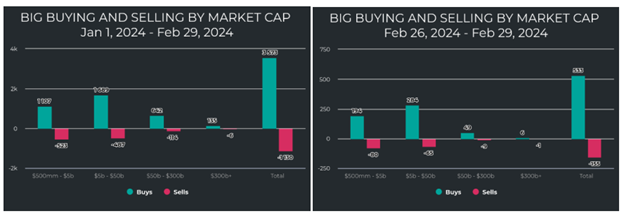

It’s also worth pointing out that most of the unusually large inflows, both since the start of 2024 and continuing through the end of February, are concentrated in small- and mid-cap stocks. That reflects a consistent focus on growth stocks:

The growth orientation can also be seen in sector strength. The sectors that drive economic growth, like technology, industrials, financials, and discretionary, continue to lead the way. Meanwhile, defensive sectors are dragging:

Of course, it's only human to wait for the next shoe to drop. However, that doesn't help us emotionally, psychologically, or as investors looking to build wealth.

It's better to understand the environment, plan accordingly, and shift as needed. The fact remains that the market is strong, earnings continue to shine, and other than some strategic profit taking, the data still supports remaining steady. As of now, we’ll stay invested in what’s working.

* Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.