This post will deviate slightly from our usual economic and fundamental updates to discuss what we think is a generational wealth building opportunity that is currently underway. This is important from an investment standpoint because sometimes it pays to focus one’s due diligence efforts on a secular wave that can add multiples to one’s net worth.

We're talking about the AI revolution. We think it’s as big, if not bigger than the rollout of the internet. And it’s creating the largest wave of IT spending of all time.

According to data research & analytics company IDC, by the end of this year companies will have spent 26.5% more on AI tools than at the same time last year. Perhaps more significantly, this rate of annual growth is expected to continue at least through 2026.

Furthermore, worldwide AI spending is projected to double to over $300 billion by 2026 just in private sector expenditures alone. The U.S. will be the largest market with more than 50% of all AI-centric spending. Here’s the kicker: as we near the halfway mark of 2024, AI spending is already approaching those 2026 forecasts.

We’re seeing AI spending accelerate in a wave of fear of missing out (or FOMO). It’s almost as if a company doesn't have a state-of-the-art AI platform in place, it may as well order the last words on its corporate tombstone.

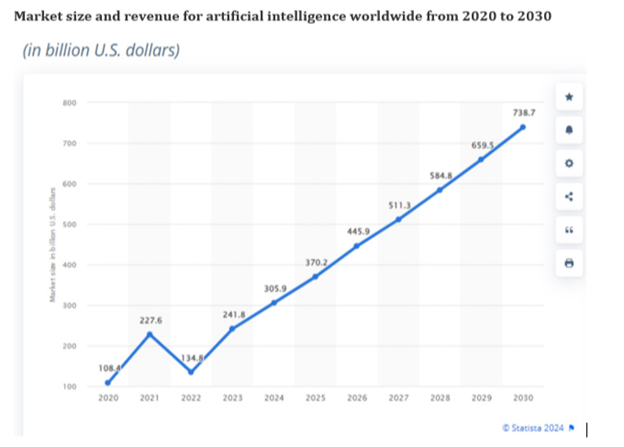

Forecasts predict $1 trillion-$2 trillion will be invested in AI by 2030. Consequently, it will lead to AI contributing up to $16 trillion to the global economy by then.

These are staggering numbers. Even more amazing is the beginning of this spending wave is happening in what some would call a “stealth” bull market.

Importantly, the AI market doesn’t care about things that can derail investments, like U.S. elections, geopolitical strife in the Middle East or Ukraine, climate change, political upheaval in Europe, and so on. It’s a unique part of this evolution. The AI battleground is simply survival of the fittest between the biggest companies in the world.

Large-cap, AI-driven technology is the here and now. So, it’s vital for us as investors to recognize this from a portfolio construction standpoint. As with most technologically disruptive mega waves, the stocks that stand to benefit the most get priced to over-perfection at some point before the spending wave matures. However, we’re currently nowhere near that stage:

As evidence that we’re still in the early stages of this evolution and not “overpriced” as some analysts suggest, let’s drill down on supportive objective data showing continued multiyear tailwinds still to come. Looking specifically at semiconductors, which we view as the “picks and shovels” of the AI evolution, there are three recent developments that exemplify continued support of buying AI-centric equities.

First, at its recent development conference, Apple Inc. (AAPL) knocked the cover off the ball, showing how Apple Intelligence will be brought to the masses later this year. Keep in mind, Apple is one of the most important companies on the planet and it’s a late participant in the AI game.

Second, the May consumer price index came in lower than expected. This provides continued bullish tailwinds due to inflation’s downward trend.

And third, recent mega earnings announcements from tech stalwarts like Oracle Corp. (ORCL) and Broadcom Inc. (AVGO) continue to prove how large-cap tech companies are nowhere near earnings growth peaks.

With high quality tech stocks reaching new heights, some investors may be inclined to think tech companies have gotten ahead of themselves. We respectfully disagree and will show why there’s more tech upside.

One Direction for Share Prices to Travel

Day after day we’re greeted by companies blowing past earnings estimates. The best example of this is from the newly crowned king of the market, NVIDIA Corporation (NVDA). Its most recent earnings report showed $28 billion in quarterly revenue, easily outpacing estimates of about $26.62 billion.

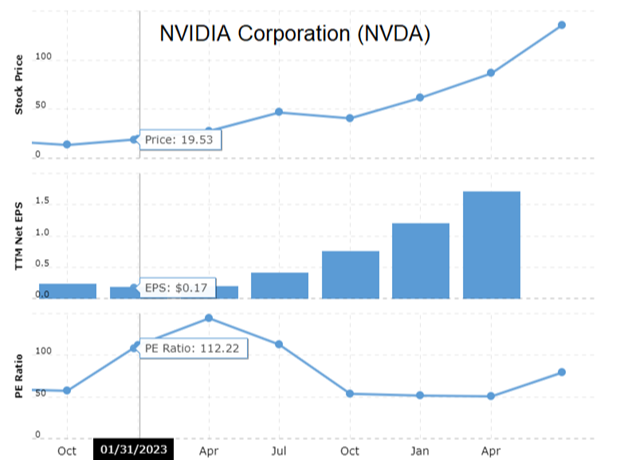

Some may think NVDA is now too expensive. But even with its massive market growth, from a price-to-earnings standpoint, the company is actually cheaper today than it was in January 2023:

Adjusting for its recent stock split, on Jan. 31, 2023, NVDA’s price-earnings ratio was 112.22, with per-share earnings of $0.17. As of this writing, the P/E ratio is 74.63 with earnings of $1.71 per share. Furthermore, NVDA’s forward P/E ratio currently sits at only 49.15.

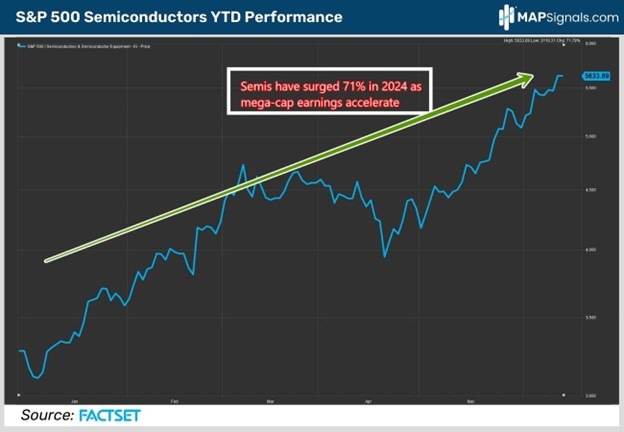

With earnings growth like that spread across the semiconductor industry, there's only one direction for share prices to travel, and that is up. Semiconductor firms have gained a staggering 71% in 2024 alone:

We think this can continue for three reasons.

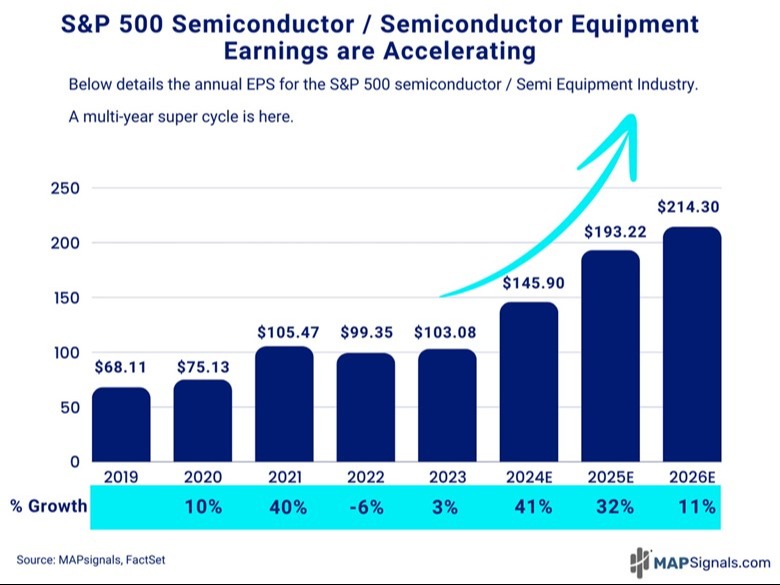

The first is simple: stocks follow earnings. Not only have earnings been climbing, they’re also set to explode in the future:

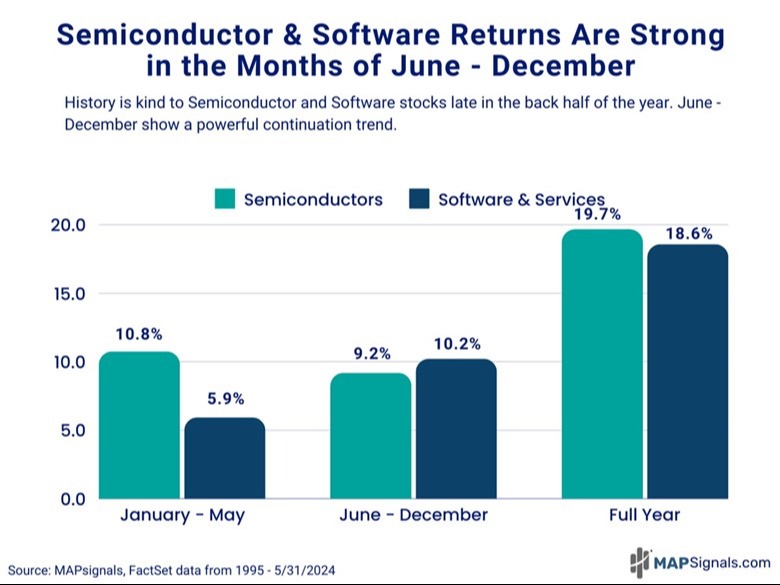

Next, history suggests jumping off the semiconductor bull wagon this summer would be a mistake. June typically kicks off a bullish trend through the end of the year for the sector. Since 1995, semiconductors gained an average of 9.2% in the final seven months of the year:

Earnings picture bright? Check.

Sound technical picture? Check.

To drive this home, let’s review institutional money flows, which our readers know drives markets overall. This is the third reason we think semiconductors keep running.

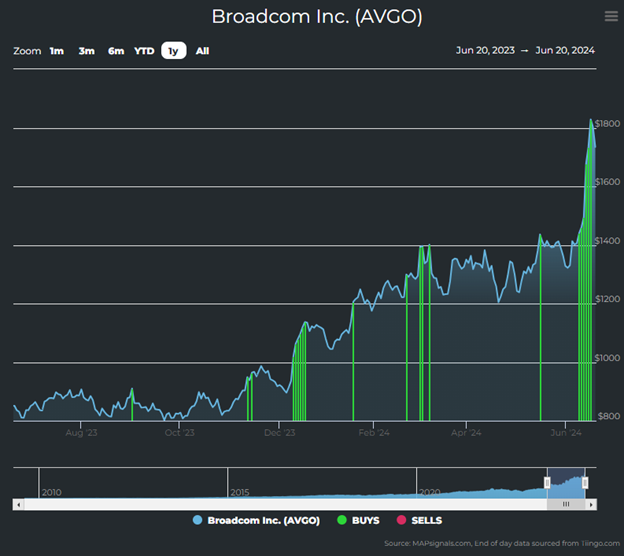

With the recent explosive earnings report from Broadcom, which we’ve owned in client accounts for more than three years, it’s appropriate to examine “big money” interest in the company. It exemplifies the bigger picture via individual stock analysis.

Each green bar below shows institutional money inflows. Clearly AVGO is a “big money” favorite:

The green bars lift the share price over time. This type of action is what we look for in our quantitative data research. The institutional demand for this incredible company has made it a mainstay in our research.

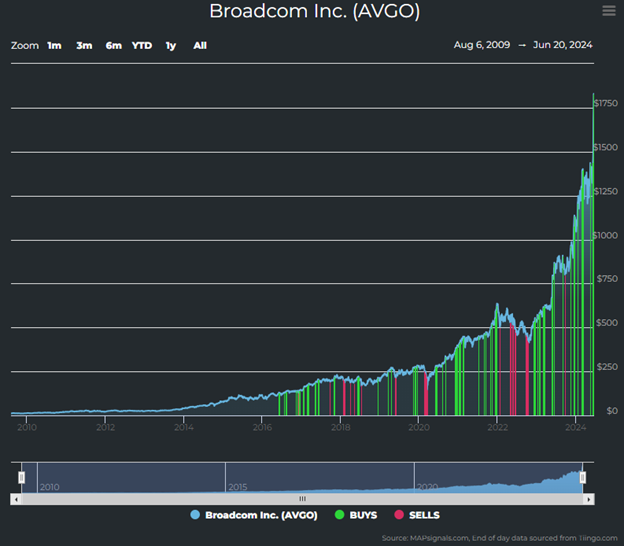

Zooming out, it’s clear AVGO’s institutional demand has been there for a long time:

This is the perfect example of an outstanding semiconductor company that is poised to continue to climb simply due to the ultimate power law in markets – relentless demand drives returns.

In summary, the earnings picture for this industry is bright, it has technical tailwinds, and there’s strong institutional demand. This scenario provides the foundation for us to philosophically continue to position our client portfolios for further upside in semiconductors because of the AI super cycle that’s already here.

* Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

* AAPL, ORCL, AVGO, and NVDA are owned in Cornerstone client accounts and by Daniel Milan personally.