Let’s get the “topic du jour” – the federal government shutdown that began last Wednesday at 12:01 a.m. Eastern Standard Time – out of the way.

While it’s a fun headline-drawing event for news organizations, we at Cornerstone think this will be a sidebar issue from an investment perspective, just as with previous shutdowns. There will be little if any effect on the probabilities that heavily favor continued strength in stocks for the remainder of the year.

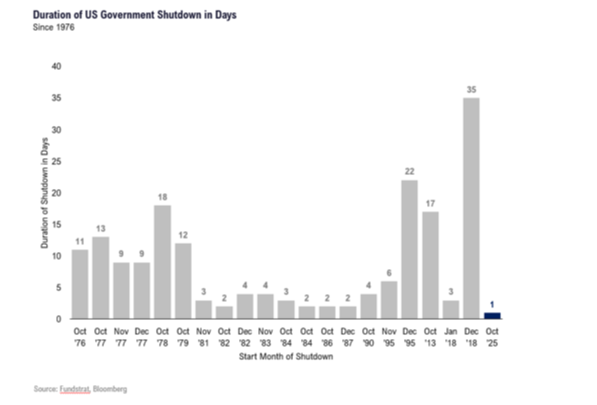

Sure, some pundits may scream from the hilltops about any protracted shutdown being disastrous. But look at 2018, when the government shut down for 35 days, the longest span in recent history:

Even then there was no material economic or market impact.

It's important to acknowledge that any protracted government shutdowns will have a short-term negative effect on the economy. Once the government reopens, furloughed federal employees receive all the back pay owed to them that accrued during the shutdown. In other words, they’ll get paid eventually.

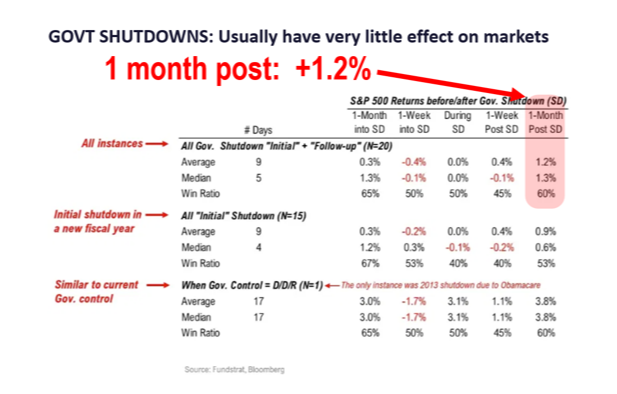

Understanding history provides us with the confidence to not lean bearish merely because of governmental shutdowns. They simply haven’t created lasting impacts on equities:

Even if stocks dip in the short term, we consider it an opportunity to buy. More importantly, it's critical to focus on how we’re entering the seasonally strongest period of the year.

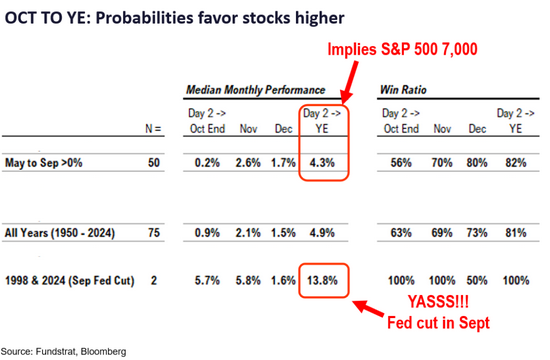

As we detailed last week, even in the face of this governmental shutdown, the setup significantly favors strength in equity markets, so much that current probability data implies the S&P 500* will hit 7,000 by year end:

As the adage goes, this would be one of those times to “see the forest through the trees” and maintain a long-term view.

The Compounding Effect

Let’s now to turn to perhaps our favorite topic here at Cornerstone: dividend growth stocks. Sometimes dividends can be easy to overlook when the market rips higher, as it has for the last six months. But as our readers know, it's important to always be looking ahead.

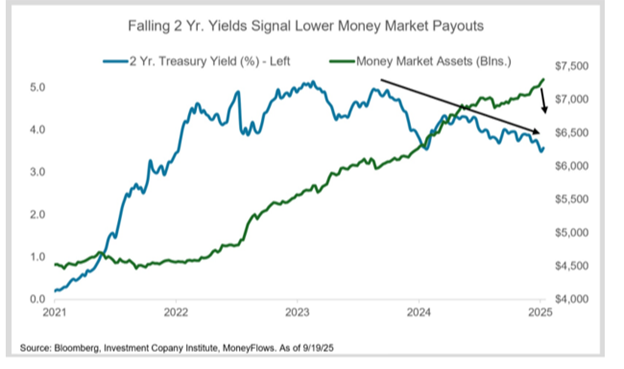

To that end, a clear setup is strengthening for equity income strategies as interest rates continue to drop. Simply put, interest rate cuts favor dividend stocks.

As of this writing, the fact that the two-year Treasury sits at 3.58% continues to imply two additional rate cuts by 2026. This is important because it will have a direct effect on the risk-free money market interest rate.

As an example, just last week the Schwab Prime Advantage Money Fund (SWVXX) yielded 3.98%. Our expectation is for that rate to settle in around 3.5% by 2026.

There’s a big difference between earning 4.5% at the beginning of 2025 and getting 3.5% or less in the first half of next year.

In rate cutting cycles like this, historically, we have seen big outflows from money markets into dividend equities. That becomes even more powerful when you remember dividends are taxed at 15% in comparison to the interest from money market accounts, which is taxed at higher ordinary income rates.

Aside from mere rate and tax benefits, when you reinvest dividends, you're also investing a growing amount every year. For example, S&P 500 dividends have compounded at a 7% growth annual clip since 2000. In Cornerstone’s dividend growth model, we specifically target an average weighted annual yield growth rate of 7% to 10%.

This compounds much faster than you’d think. For instance, in 2025 the S&P 500 constituents are forecasted to pay off a record $685 billion in dividends. That’s up from the $136 billion paid out in 2000 (an increase of 403%).

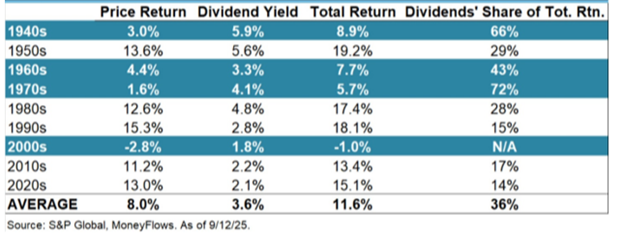

This is why the compounding effect of dividends accounts for an almost unbelievable 36% of the total long-term S&P 500 return:

Another way to look at it is the S&P 500 has returned 8% a year without dividends (price return) versus an 11.6% average total return when dividends are reinvested. Furthermore, notice in the highlighted rows above how dividends act as a shock absorber of sorts in periods of market weakness.

This data is why dividend growth investing provides higher risk-adjusted returns, which quite frankly is the holy grail of asset allocation investing.

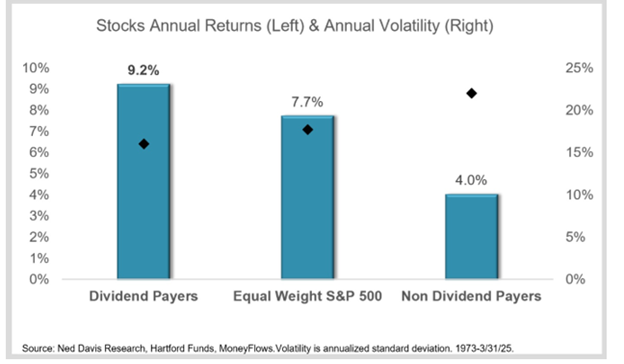

It should be no surprise that a recent study by Ned Davis Research showed that since 1973, dividend-paying companies meaningfully outperformed non-dividend payers while also being significantly less volatile:

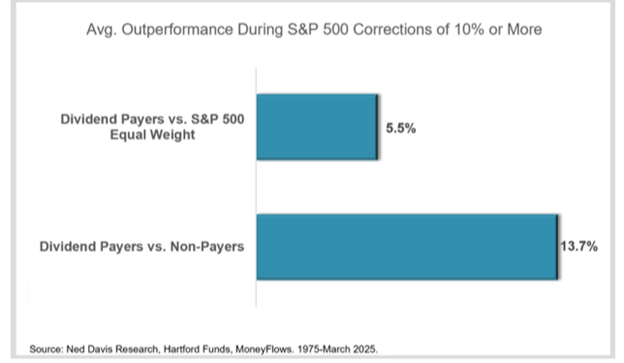

This low-volatility-driven strength becomes clear by the fact that historically, dividend-paying stocks have held up better than non-dividend payers during periods when the S&P 500 fell 10% or more:

Also, since 1975, during major market drawdowns, dividend paying stocks declined 14.4% versus non-dividend paying stocks falling an average of 28.2%. Just earlier this year this played out. During the tariff tantrum from March 15-April 15, our dividend growth model allocation only dropped 2.5% while the S&P 500 cratered.

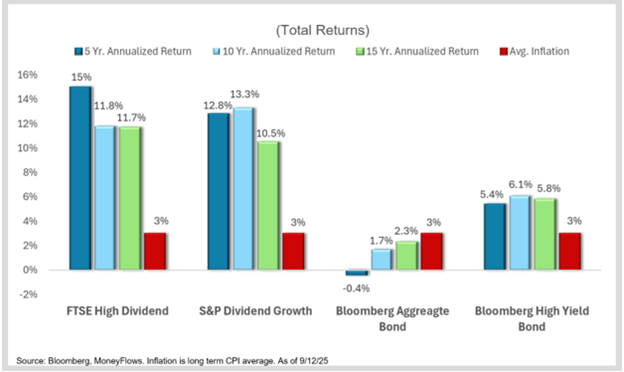

Putting a bow on this dividend love fest, let’s also highlight the strong argument that dividend equities are a more appropriate risk management tool than traditional bond allocations. Over the last 15 years, the Bloomberg U.S. Aggregate Bond Index hasn’t even matched average long-term inflation:

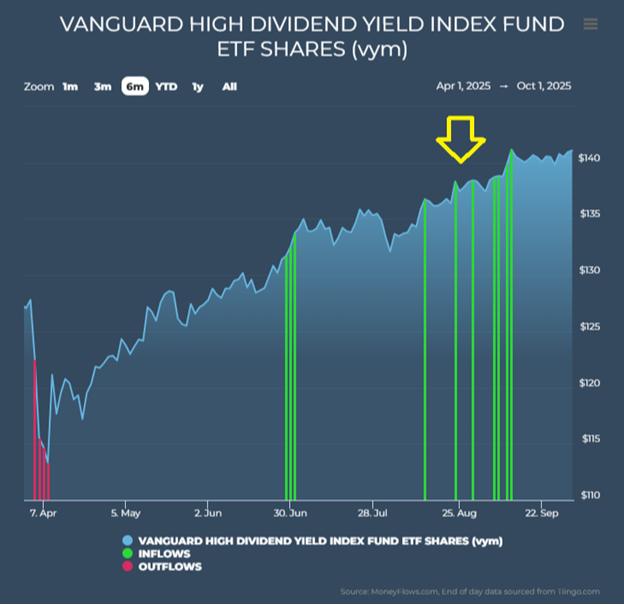

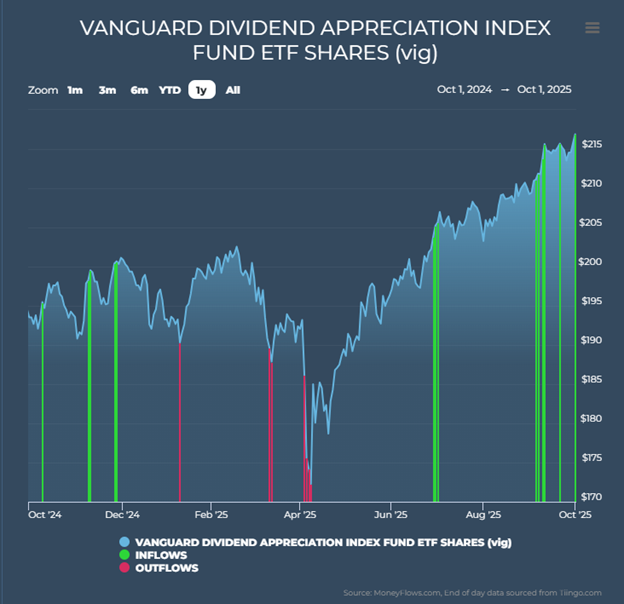

As we enter this new rate cutting cycle, a pattern is clear: institutional money is once again leading the pack by executing a dividend equity investment thesis. Using two of the largest and most popular dividend exchange-traded funds as examples (VYM and VIG), you can see how large institutional inflows into both ETFs began before August:

This action has driven ample price growth for both funds in the last two months. This is clear, heavy institutional accumulation at work.

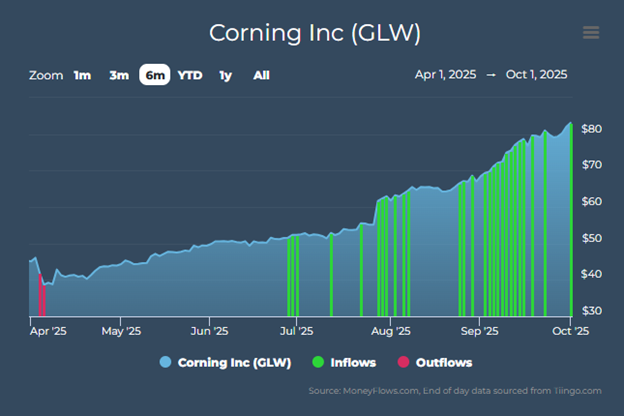

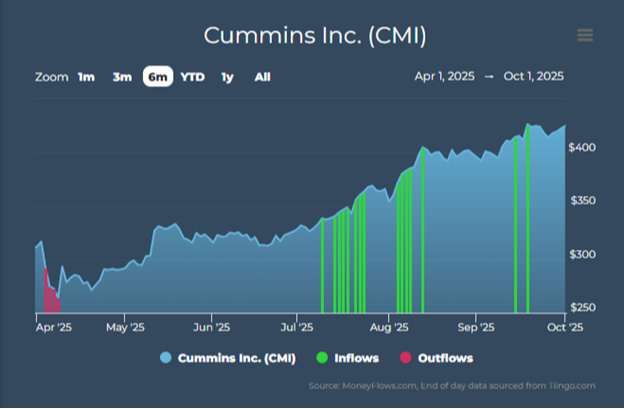

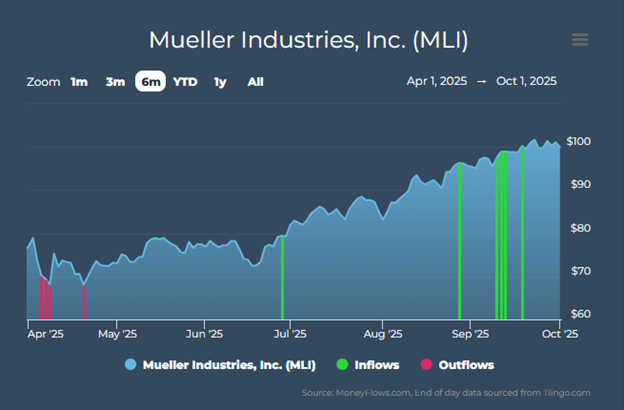

Just for fun, we dove deeper to show the below three stocks owned in our dividend growth model^. Green shoots of institutional accumulation occurred at the same time as the ETF buys:

This clear money flow data shows the beginning of a trend of dividend payers being favored by institutions to outperform. So, as the Fed keeps cutting rates, there remains a strong foundational underpinning to lean into compounding, dividend-paying stocks.

* Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

*Past performance does not guarantee future results.

*Investing involves risk and you may incur a profit or loss regardless of strategy selected.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

^ GLW, CMI, and MLI are owned in Cornerstone client accounts. Daniel Milan does not own them personally.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.