Now that earnings season has wrapped up, it’s time to turn our attention to what the current fundamental data says we can expect looking forward. This is especially interesting considering some of the popular bearish narratives about higher oil and gas prices, rising interest rates, valuations, etc.

The first data we want to review is analyst expectations going forward. After the amazing run stocks have enjoyed for the past two months, are analysts lowering their expectations more than normal for the second quarter?

The short answer is no.

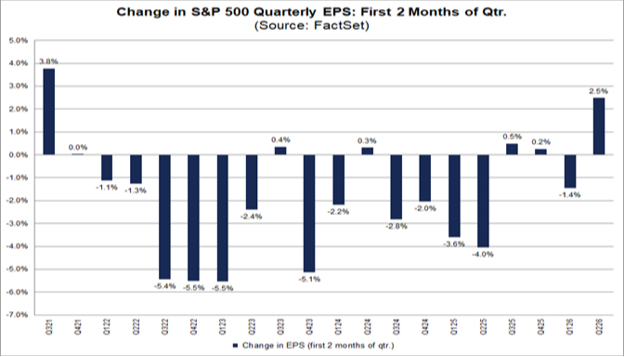

During April and May, analysts actually increased per-share earnings estimates for Q2, with the current bottom-up EPS estimate calling for an increase of 2.5%:

This is especially interesting because analysts usually reduce earnings estimates during the first two months of a typical quarter. For example, look at the average declines in bottom-up EPS estimates during the first two months of a quarter at various time frames:

- Five years, -1.6%

- 10 years, -2.2%

- 15 years, -2.6%

- 20 years, -3.2%.

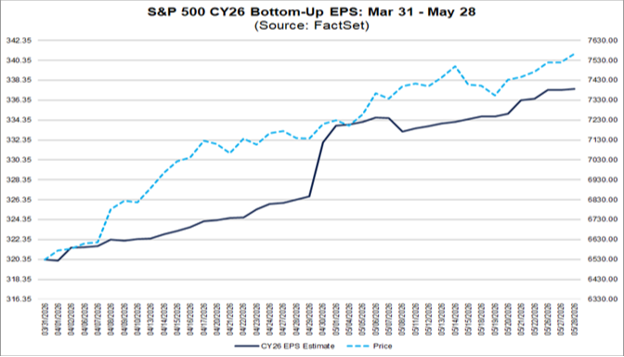

Furthermore, expanding analyst bottom-up EPS estimates throughout the rest of 2026, they’ve increased by 5.3% over the past two months:

From a historical comparison perspective, what we’re seeing is unprecedented. Keep in mind, analysts are extraordinarily conservative by nature.

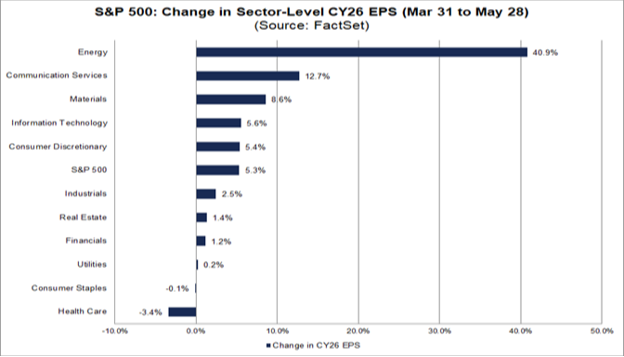

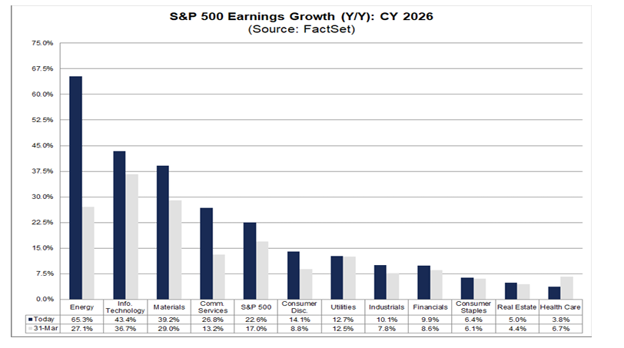

Additionally, these earnings increase expectations are not consolidated to merely a couple of sectors. It’s broadly distributed:

Armed with these extraordinarily bullish fundamental expectations for the remainder of 2026, today let’s outline a path for the S&P 500 to blow past initial expectations.

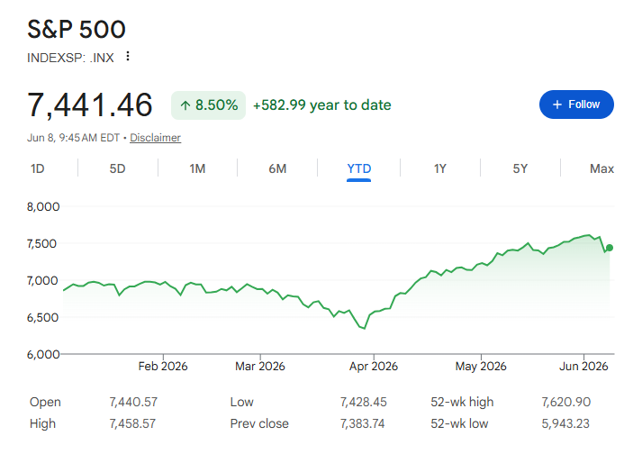

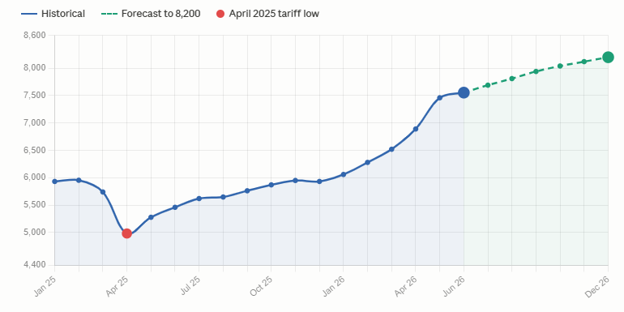

Some may think it's time to cash out. But we at Cornerstone believe the current objective data requires us to raise our initial year-end target for the S&P 500 from 7,700 to 8,200. This revised target indicates a roughly 10% increase to the current position by year end:

Building on the increased analyst EPS expectations, let’s now examine three specific macro data sets that are the driving forces behind our upgraded expectations.

Rising Interest Rates, Current Economic Setup Won't Be Headwinds for Stocks

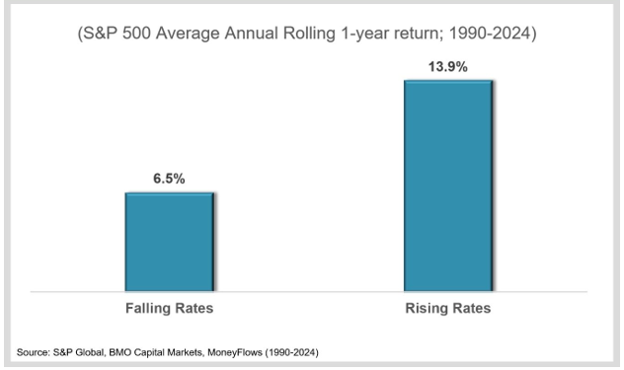

You’ve probably heard the one recent bearish macro narrative of higher-for-longer oil prices meaning significantly higher inflation and rising interest rates that will doom “overpriced” stocks. But it’s imperative to determine why longer-term interest rates are rising.

See, the market reacts differently depending on whether longer-term bond yields are increasing due to economic expectations weakening or strengthening. This distinction is important because going back to 1989, stocks have performed better when they rise alongside increasing bond yields if the market is expecting overall fundamental strength.

As mentioned, corporate earnings are setting records. When combined with increasingly strong economic expectations for the remainder of the year, it suggests the recent 10-year Treasury yield rise is for the right reasons (i.e., strong growth not spiraling inflation).

Importantly, the increase in the 10-year yield coincided almost exactly with when earnings came out, showing strength in the market.

Earnings, Earnings, Earnings – the Gas that Fuels the S&P 500 Much Higher

As we know, stocks follow earnings.

It’s important to recognize that even in the face of higher oil and energy prices, earnings growth has remained extraordinarily resilient. While it may seem like beating a dead horse, we can’t overstate how critical it is that even in the wake of a historically strong Q1 earnings season, it’s clear this level of earnings growth isn’t a blip on the radar.

It looks like the beginning of a multi-year earnings explosion.

First and foremost, analyst revisions for 2026 EPS growth are now up to 22.6% year-over-year:

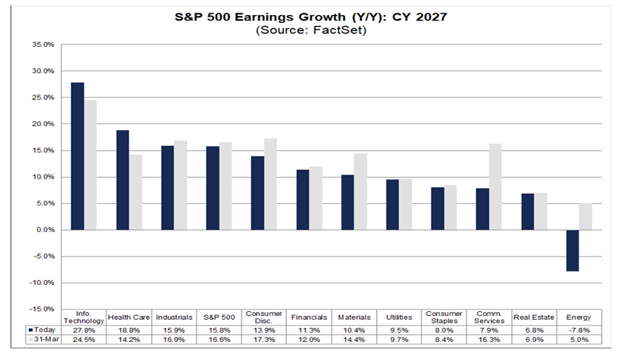

Furthermore, analysts expect this earnings growth bonanza to extend into 2027:

That healthy 15.8% index expectation is even more astonishing when you consider the 10-year EPS growth average is 10.3%. Also, if 15.8% happens, it’s on top of what occurs this year.

This surge in earnings expectations for the next couple of years is the foundational support necessary to see a path forward where valuations can continue to be attractive, even as we hit new highs.

Valuations Become More Attractive as Earnings Increase More Than the Price

It feels like we’ve heard the bearish pundits talk about stretched valuations for years now. Frankly, fundamental earnings data doesn’t support this viewpoint.

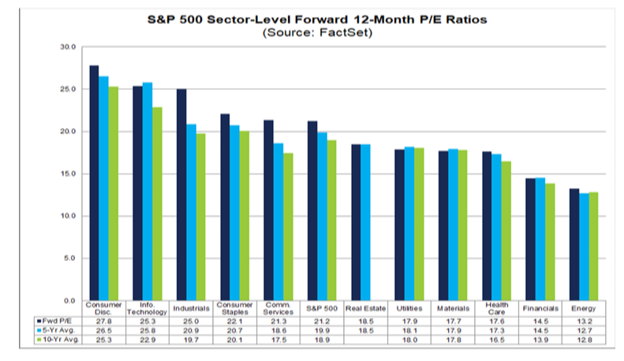

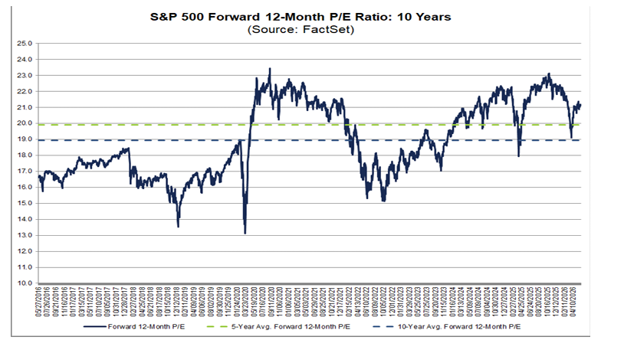

Even with the S&P 500’s amazing rip since April 1, the 12-month forward price-earnings ratio sits at just over 21 times.

Crucially, this forward P/E valuation is down from 23 times earlier this year due to the explosive increase in earnings, which have risen significantly more than the stock prices.

This valuation attractiveness is further supported by the fact that this explosive earnings growth is happening as the P/E-to-growth ratio (PEG ratio) is under 1x:

From a valuation perspective, any PEG ratio below 1x is considered a sign that the current market price is undervalued. Comparatively, the 10-year average PEG ratio for the S&P 500 is about 1.32x.

Visualizing this differently, note how the forward P/E (far right) contracted this quarter even as stock prices broke out to new highs:

This data directly contradicts the popular “stretched valuation” narrative.

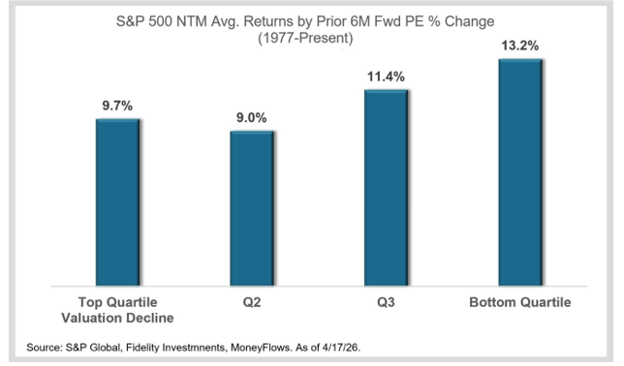

Lastly, significant valuation contractions similar to what we have experienced over the past couple of months have tended to set the stage for strong equity advances over the following 12 months:

Putting everything together, the current data environment, strong price momentum, better-than-feared macro backdrop, record earnings, and reasonable valuations clearly indicate the S&P 500 has plenty of room to run.

That’s why we felt it prudent to update our year-end price target from 7,700 to 8,200. Hitting that target doesn't require much P/E expansion and is instead fully supported by earnings-driven growth.

*Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

*Past performance does not guarantee future results.

*Investing involves risk and you may incur a profit or loss regardless of strategy selected.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.