Early last week, adverse emotions crept into the market.

This was evident in long-term yields inching higher and the CBOE Volatility Index (VIX), a measure of market volatility, gaining over 20% on Monday and Tuesday (April 1-2). These moves forced a negative start to the quarter for the S&P 500*, Nasdaq Composite Index#, and Russell 2000^ as volatility emerged throughout the week.

So, we’re keying in on three short-term catalysts:

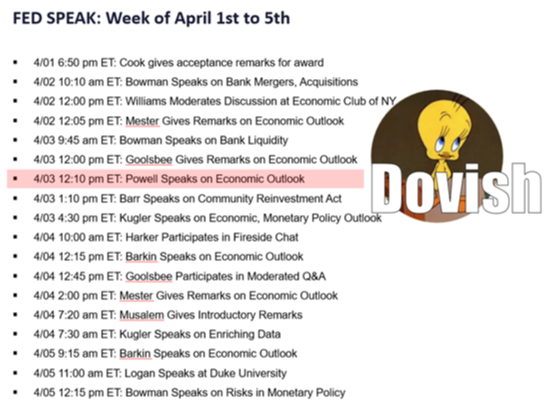

- Last week Federal Reserve Chair Jerome Powell continued his cautious-yet-doveish tone, which is consistent with his recent post-Fed-meeting commentary and Congressional testimony. His speech was part of a “Fed speak” flurry to begin April:

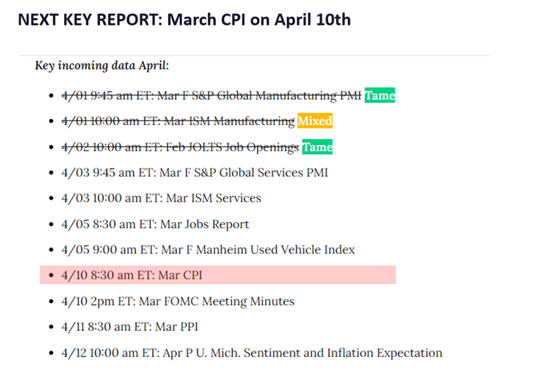

- On Wednesday, a key inflation metric – the March consumer price index – will be released:

- We think there’s a strong probability the CPI is lower than Wall Street’s consensus expectation of a 0.3% increase because early indications from Europe are extremely soft, highlighting the statistical aberrations of the January and February reports.

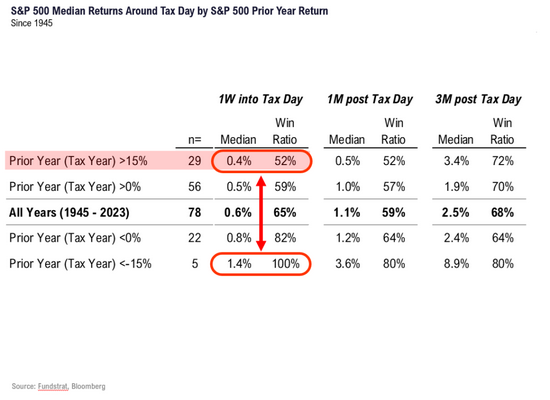

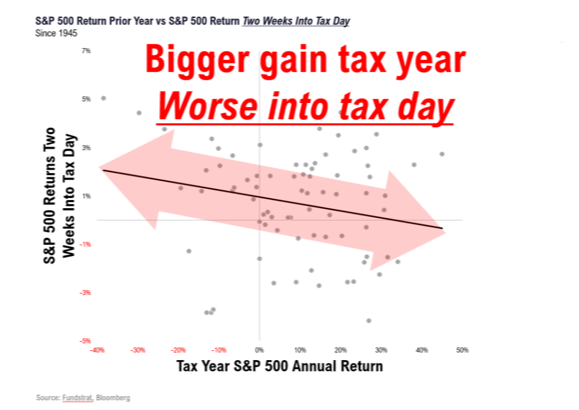

- Some of the softness from early last week is likely due to tax-related selling pressure on stocks that historically continues through this week leading up to Tax Day (investors need to raise cash to pay capital gains taxes). It’s an annual mechanical issue that dissipates quickly.

This action may toy with people’s emotions. But as our readers know, we believe emotions taint objective views on markets and investing.

Currently, some would argue the stock market defies logic. But does the market defy logic, or emotion?

Possibilities and Probabilities

Let's begin by reviewing the market since November. It looks almost unnaturally uniform in its steady uphill climb:

Understandably, it's human nature to wait for the next catastrophe. The trend in that chart can't last forever, right? But is it possible the market will keep going?

The answer is yes, it’s possible.

Is it probable? No, though the possibility remains that it could.

This seemingly improbable bull run is nothing new, especially when compared to the last eight years:

All those tight, upward channels reinforce how it's wise to be unattached emotionally, focusing on objectively pure data.

What does the data say now?

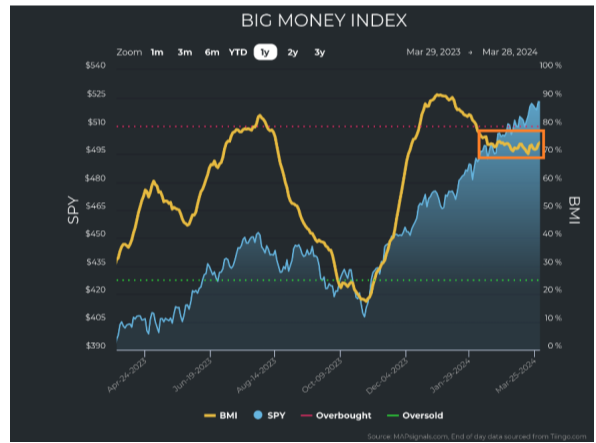

Our readers know we think the best objective indicator of market activity is MAPsignals’ Big Money Index (BMI), a 25-day moving average of netted buys and sells by institutional “big money” investors. The BMI says to relax and enjoy the ride. It’s been tightly sideways since falling from overbought territory in February:

History told us to expect market weakness when the BMI dropped from overbought. We’ll be ready if it does, especially now that we're in the earnings “dead season” that begins each quarter. But that weakness hasn’t happened yet.

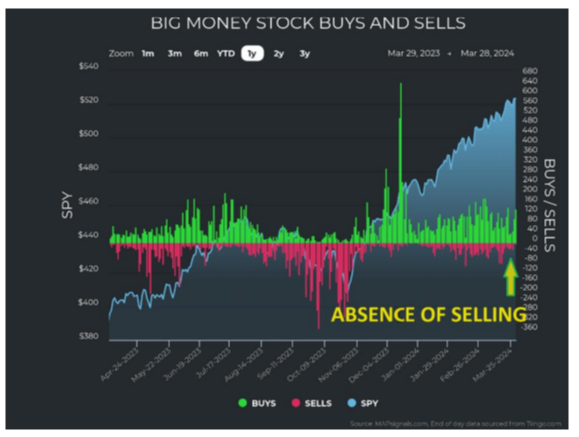

The reason why is found by analyzing data beneath the surface. Although buying fell from extreme December levels, unusual selling never increased:

If selling ramps up, we’ll be ready because of our laser-like focus on data and ability to cast emotion aside.

Every quarter starts with a lack of earnings announcements and thus minimal trading catalysts, meaning volatility can rise (perhaps because investors are left to their emotions). Thus, we want to be especially cognizant of the data we do have available during these times.

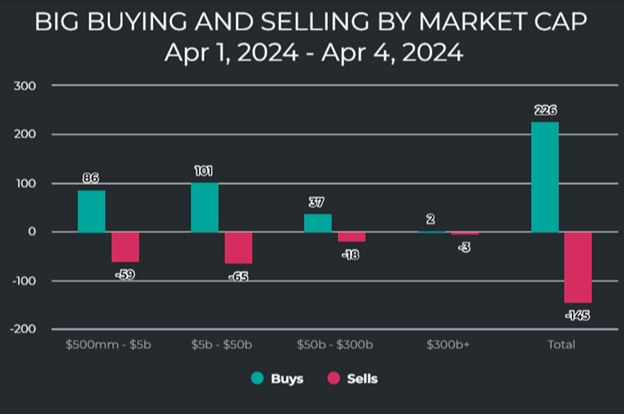

Interestingly, even with the day to day volatility last week we can see there has still been more buying:

This data fuels the possibility of a continued bull run. Furthermore, sector analysis is upbeat:

- All 11 sectors charts are strong, with no weak links in the chain:

- A simple eye test of the charts above reveals no worrisome selling in any sector. While communications may look bad, inconsistencies since that sector came out in 2018 mean there are so few stocks in it (only 79 of 5,500 stocks we review – just 1.4%), that any concerns are irrelevant.

- We probably can all agree the technology sector – humanity’s advancement driver – holds the key to sustained growth. The chart below indicates a potential inflection point – will extreme buyers return or will selling take over? Only time will tell.

This is what we’ll be watching most closely in the next few weeks.

Stocks are Partying Like It's 1995

As we begin to analyze the new quarter data, it would behoove us to recognize how the first quarter unfolded with brief, shallow pullbacks. From a historical perspective, stocks are partying like it's 1995.

While foolish to extrapolate one quarter into a whole year, 2024 so far does resemble 1995 and the only economic “soft landing” engineered by the Fed in recent history. Back then, the central bank began cutting rates after raising them for a year, adding rocket fuel to the stock market – the S&P 500’s total return that year was 37.1%.

Oddly enough, the rate cutting cycle that began in 1995 had three cuts. There’s been some hawkish tones from Fed members, but the latest Fed dot plot shows three cuts are pretty much the plan for 2024.

Looking at the chart of the inflation-adjusted S&P 500, if interest rates were to decline like in 1995, it's clear we could see further appreciation for stocks from here:

If a 1995-like pattern unfolds, we're currently at its beginning stages. Further supportive evidence comes from The Conference Board’s Index of Leading Economic Indicators (LEI). It’s been forecasting a recession that “never came” for a long time (or did it, but in a rolling fashion?).

Last month, this indicator trended positive. While still technically negative, it’s risen steeply from a depressed level. After steep rises in the past, the index has never reversed course. In fact, now the LEI is forecasting the beginning of an economic expansion.

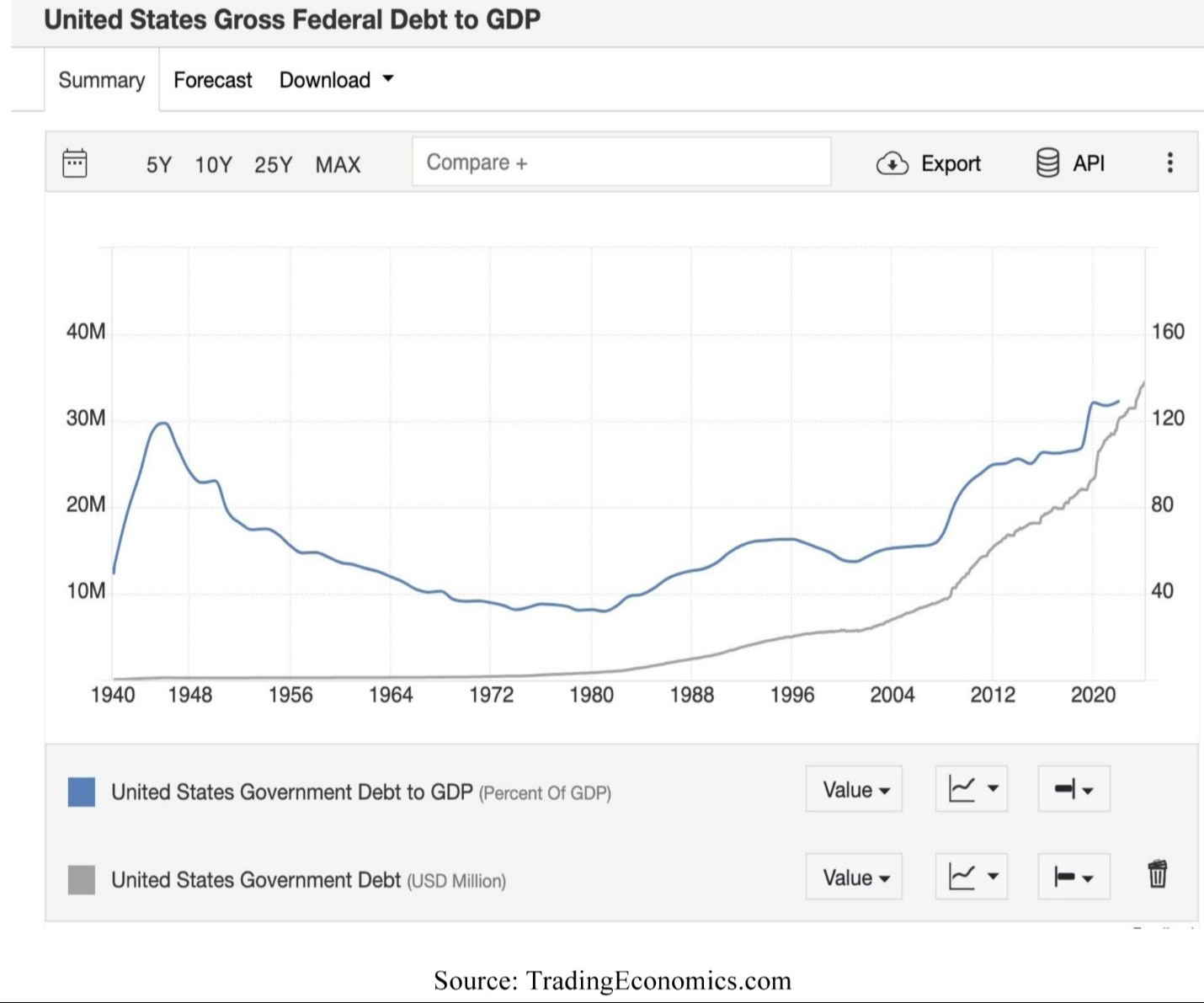

Still, there could be growth headwinds. Perhaps the most important one is government debt (but we'll address that elephant in the room another day in more detail):

A full-blown, non-rolling recession is harder to see compared to the same time last year. Maybe this is what our 1995-style “soft landing” looks like.

* Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

# The Nasdaq Composite Index is a market capitalization-weighted index of more than 2,500 stocks listed on the Nasdaq stock exchange.

^ The Russell 2000 Index is a stock market index measuring the performance of the 2,000 smaller companies in the Russell 3000 Index and is widely regarded as a bellwether of the U.S. economy.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.