Last week, the S&P 500 officially ended the first half of 2026 up about 9%. This is a great outcome, especially considering the volatile first quarter and the unexpected ripple effects throughout the second quarter due to the Iran war.

But most importantly, as was highlighted last week, even with the strong overall first half and parabolic Q2, equities are less expensive now than they were at the start of the year. Let’s examine a bit of then versus now:

- 2027 per-share earnings – $350.00 then versus $400.00 now

- 2027 price-earnings ratio – 19.4 then versus 18.4 now

- Thus, 2027 S&P P/E is 1.0x lower

Considering the typical volatility during midterm election years, the market has shown borderline astounding resilience.

Entering 2026’s second half, we at Cornerstone continue to maintain an overall constructive forward-looking view. But there are risks.

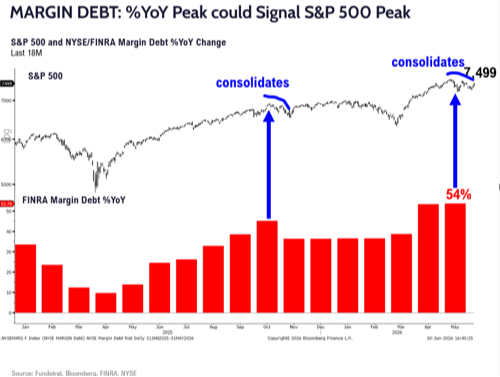

For instance, it’s prudent to point out how margin debt has now risen 55% year-over-year, which is the fifth highest rise in the past 70 years:

Prior surges like this were followed by some consolidation as markets digest the increased level of borrowing. There's a possibility this margin debt could be a contributing factor to any short-term drawdown volatility in Q3.

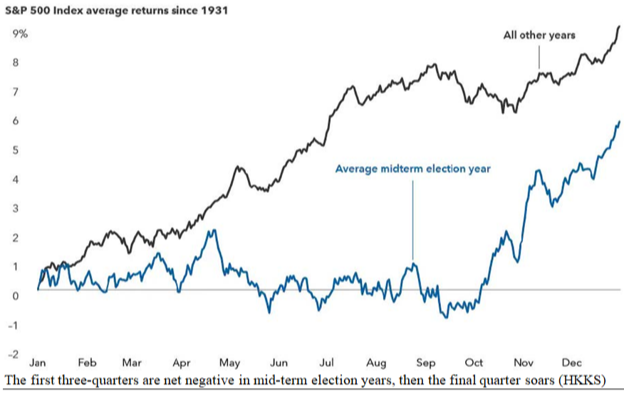

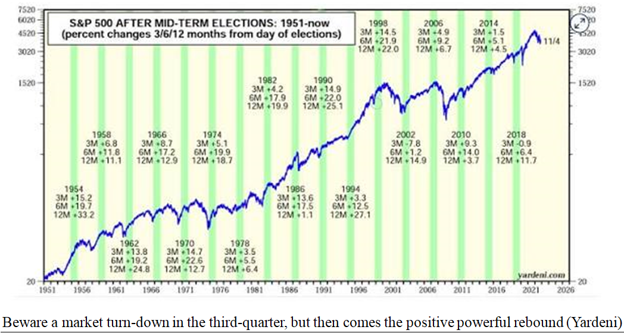

Also, we’ve mentioned many times the dismal historical track record in midterm election years, especially in the months leading up to the election. Since 1931, the difference between the S&P 500’s average return in midterm years versus non-midterm years is startling:

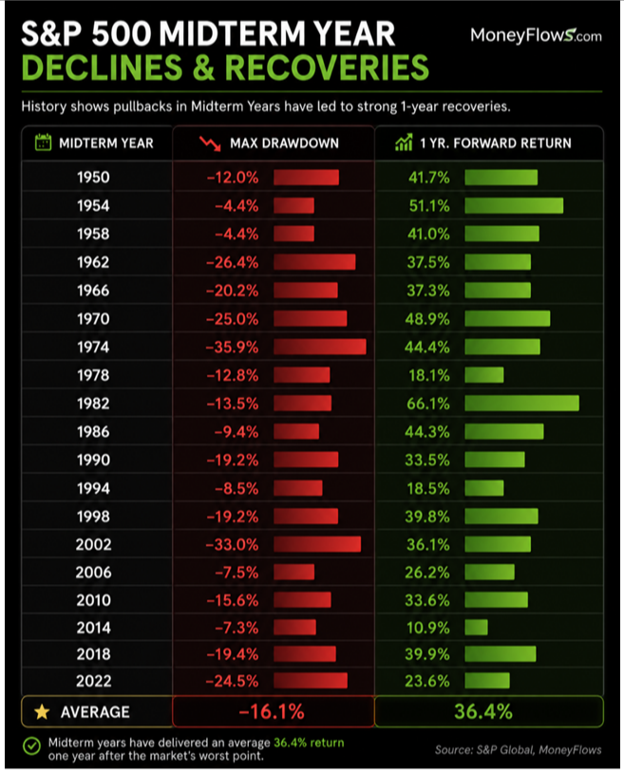

Such powerful history potentially foreshadows upcoming short-term volatility. But we want everyone to recall the crucial takeaway – the 12 months after a midterm election have never posted a negative return since 1950:

In our opinion, there's a clear contributing factor for these enormous recoveries. Simply, we know that markets despise uncertainty. The uncertainty leading up to midterm elections often creates environments that cause investors to make negative, emotional decisions. Subsequently, as certainty re-enters the picture, the negative emotions inevitably alleviate.

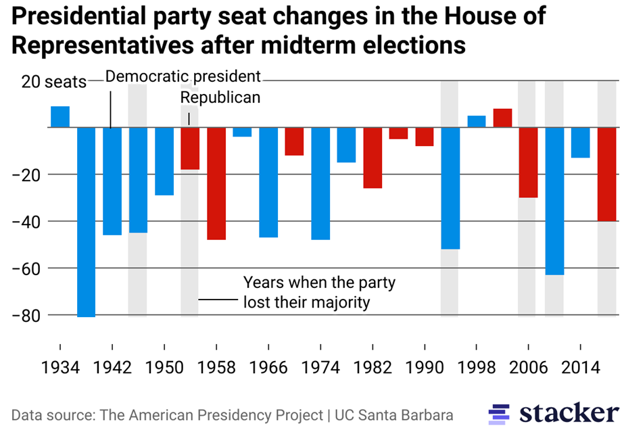

Remember too that midterm elections tend to put “restraining orders” on incumbent one-party power monopolies. For example, the last four incumbent presidents offered massive reversals of their seats in Congress, which were reflective of voters’ “veto powers.”

We don't know yet if the current administration will receive a second midterm spanking in November. But recent history showed how American voters used their “get out of electoral jail free” card every midterm election going back to President Clinton in 1994:

These reversals in congressional seats immediately create gridlock within the political environment. From a market perspective, that’s a good thing because it establishes full clarity that nothing of importance will change, which is what the market likes the most.

This is clearly reflected in the three-, six-, and 12-month returns after every midterm election going back to 1951:

While acknowledging these short-term risks, it’s also prudent to point out how this could be the year the historical president is broken. Yes, this time could be different.

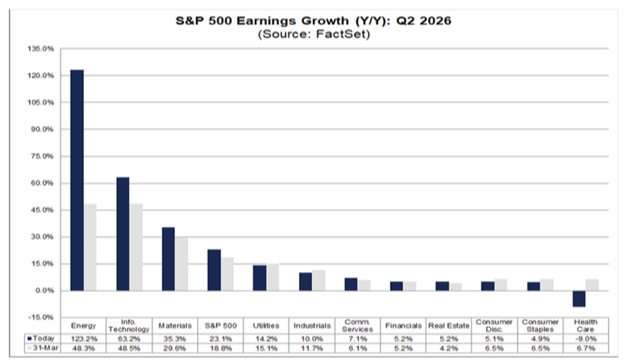

In our opinion, that possibility is because of earnings. The only thing with the power to break through electoral uncertainty is a continuation of the amazing earnings growth that we’re almost assured of experiencing when earnings season starts in a couple of weeks.

Even after last quarter's record-breaking numbers, analysts expect S&P 500 earnings to grow 23.1% year-over-year:

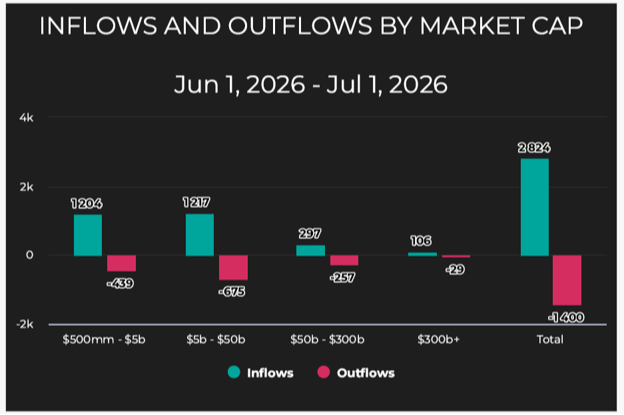

Furthermore, even as the S&P 500 was down 1% in June, the underlying money flows show how foundational support was quietly improving underneath the surface despite prices moving lower. Inflows exceeded outflows by over 2x last month:

Notice also how there were more inflows than outflows across every market capitalization level. Thus, the buying was broad.

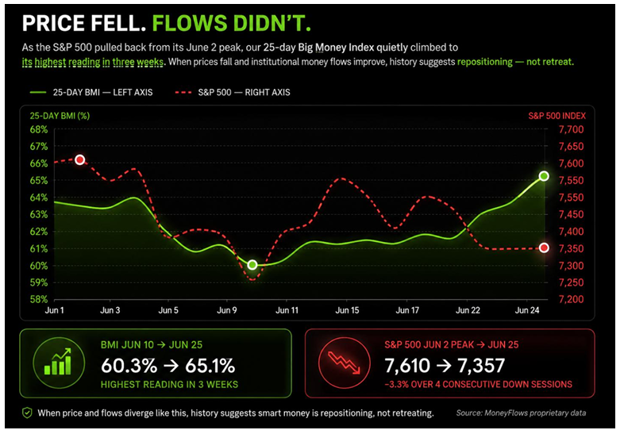

Some may point to June's market price weakness as a sign of things to come. However, historical data shows us that divergence like we saw in June indicates a market breather and repositioning in advance of an earnings season. It’s not a run for cover.

At CFS, we always prepare for risk and are prepared to make any needed adjustments. But right now, the overall picture as we enter the second half of this year continues to follow our initial 2026 outlook. If anything, the market resilience is even more impressive than we initially expected.

*Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

*Past performance does not guarantee future results.

*Investing involves risk and you may incur a profit or loss regardless of strategy selected.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.