Last week brought the first meaningful set of data since the outcome of this year’s election. That’s especially true for the Federal Reserve because, from our point of view, the October consumer price index report is the most important piece of information.

Some “bear-istas” are using the report to paint a picture of negativity. But when you look into it deeper, it’s clear this report is more favorable than it first appears. And that’s despite the fact that it was in line with expectations.

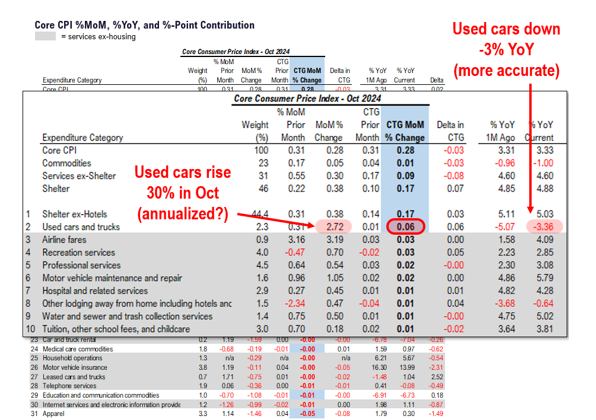

The reason for this is the 0.28% month-over-month rise in core CPI, which excludes food and energy costs, is distorted by a puzzling 30% annualized surge in used car prices. As a result, the two largest contributors to the core CPI rise were shelter, which contributed 0.17%, and used cars, which rose 0.06%:

But in reality, we all know used car prices are falling. In fact, they’re down 3% from a year ago, per the CPI data. But somehow, the October monthly rise was 2.72%, or about 30% annualized.

Does anyone actually believe this? We would argue no. We also think this distortion will disappear next month.

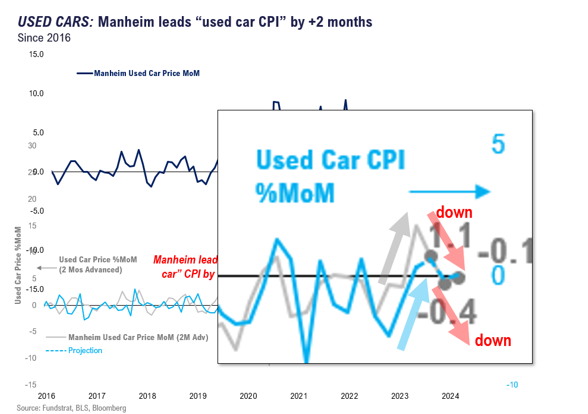

In fact, we're confident in that assertion because used cars CPI historically tends to be two months behind the Manheim Used Vehicles Value Index, which is a leading indicator of pricing trends in the used vehicle market. Based upon the most recent data, used cars CPI is likely set to fall:

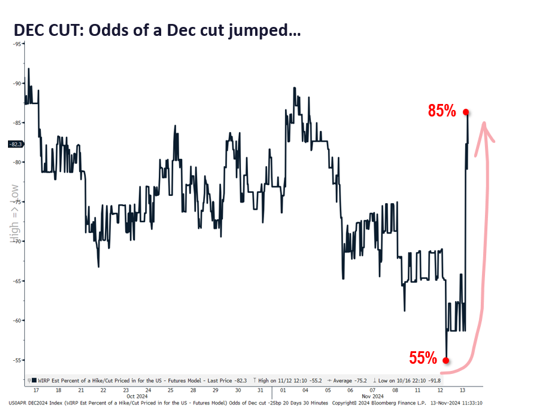

Thankfully, once the dust settled, the markets realized this as well. That fact was reflected in the odds of a December Fed rate cut. They surged from 55% to 85% quite quickly:

There’s a reason for this swift upshoot. It’s that the bond market realized the core CPI monthly jump of 0.28% should actually be about 0.22%, which is pretty close to the Fed's target.

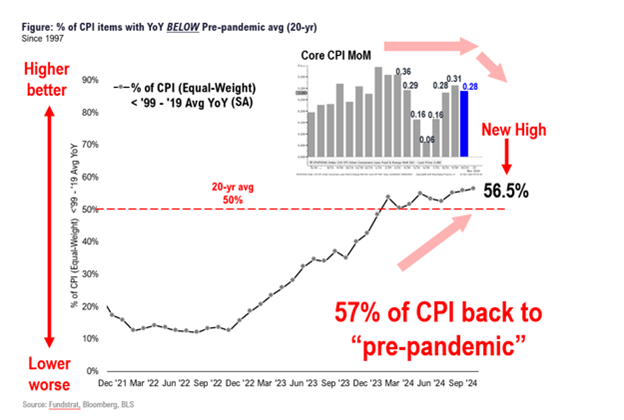

More support for this belief is that we reached a new high regarding the percentage of CPI that is back to pre-pandemic levels:

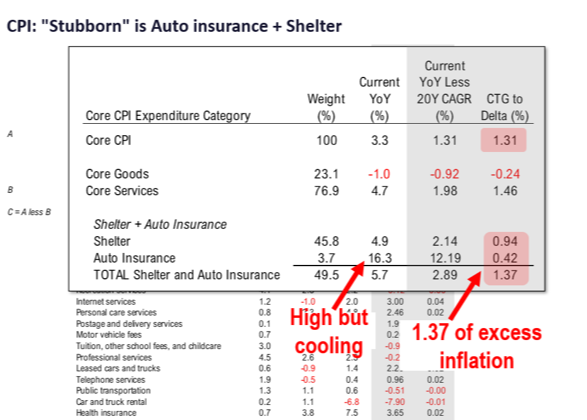

We’re still going to need some more patience though. As we’ve written about frequently, the world must wait patiently for the last two stubborn pieces of inflation to tamper down – auto insurance and shelter:

What can we do with this inflation data?

Well, when you combine the inflation data with other positive market supports, it offers an encouraging path for equities as 2024 rolls on into 2025. What other supportive market data am I referencing? I’m talking about four things, specifically.

The first is inflation. We’ve discussed how the long-term trend shows prices falling and how stubborn areas of the CPI should loosen over time. The continuation of this trend is welcome.

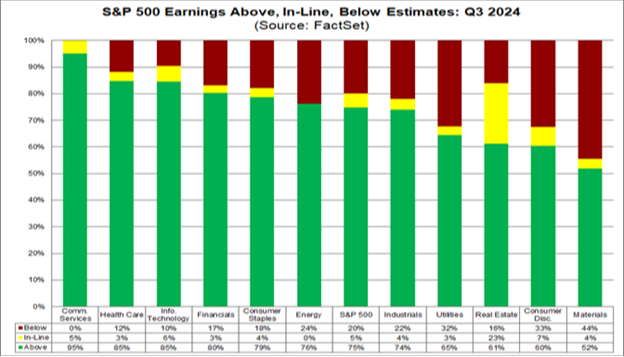

The second support has to do with corporate earnings. More precisely, per-share earnings have been incredibly resilient despite falling inflation. To date, 75% of S&P 500* companies have beat their consensus earnings estimates, which is in line with the 10-year average:

Third, the Fed continues to follow a doveish path. So, that means we’ll almost certainly see more interest rate decreases in the future.

Typically, that bodes well for stocks, especially small- and mid-cap companies that rely on financing. Cheaper debt often translates positively to the bottom line in the form of increased profits.

Finally, the newfound certainty resulting from the election has been impactful for markets. There’s been a rally since the country’s future path was determined through the electoral process, and it should continue going forward.

If it does, that most likely means the mountain of cash on the sidelines in money market accounts (totaling more than $6.5 trillion) will flow into stocks and other assets offering higher potential returns. Considering how equities valuations are still quite reasonable, the money market fund exodus may happen sooner rather than later. More buyers would obviously lift markets.

When you consider everything we’ve discussed today, is it reasonable to think markets will rise more this year?

We think so.

By how much?

Well, we think stocks will jump high enough for us to slightly reconsider the upper end of our 2024 forecast. We now think the S&P 500 could hit 6,300 by the end of this year. And if it does, it will probably be because of some (or all) of the reasons outlined above.

* Links to third-party websites are being provided for informational purposes only. CoreCap is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. CoreCap is not responsible for the content of any third-party website or the collection or use of information regarding any websites users and/or members.

*Past performance does not guarantee future results.

* The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

Securities sold through CoreCap Investments, LLC. Advisory services offered by CoreCap Advisors, LLC. Cornerstone Financial and CoreCap are separate and unaffiliated entities.